Futures Trading for Beginners: How to Get Started with Contracts

Futures trading is the direct trading of standardized futures contracts on regulated exchanges. Unlike CFDs, futures trading shows you the real order book, real volume and the real transactions of all market participants worldwide. This makes futures the preferred instrument for institutional traders and for anyone who wants to practice Order Flow Trading.

Risk Warning: Trading futures and other financial instruments carries significant risk of loss. Past performance is not indicative of future results. Only trade with capital you can afford to lose.

Why Futures and Not CFDs

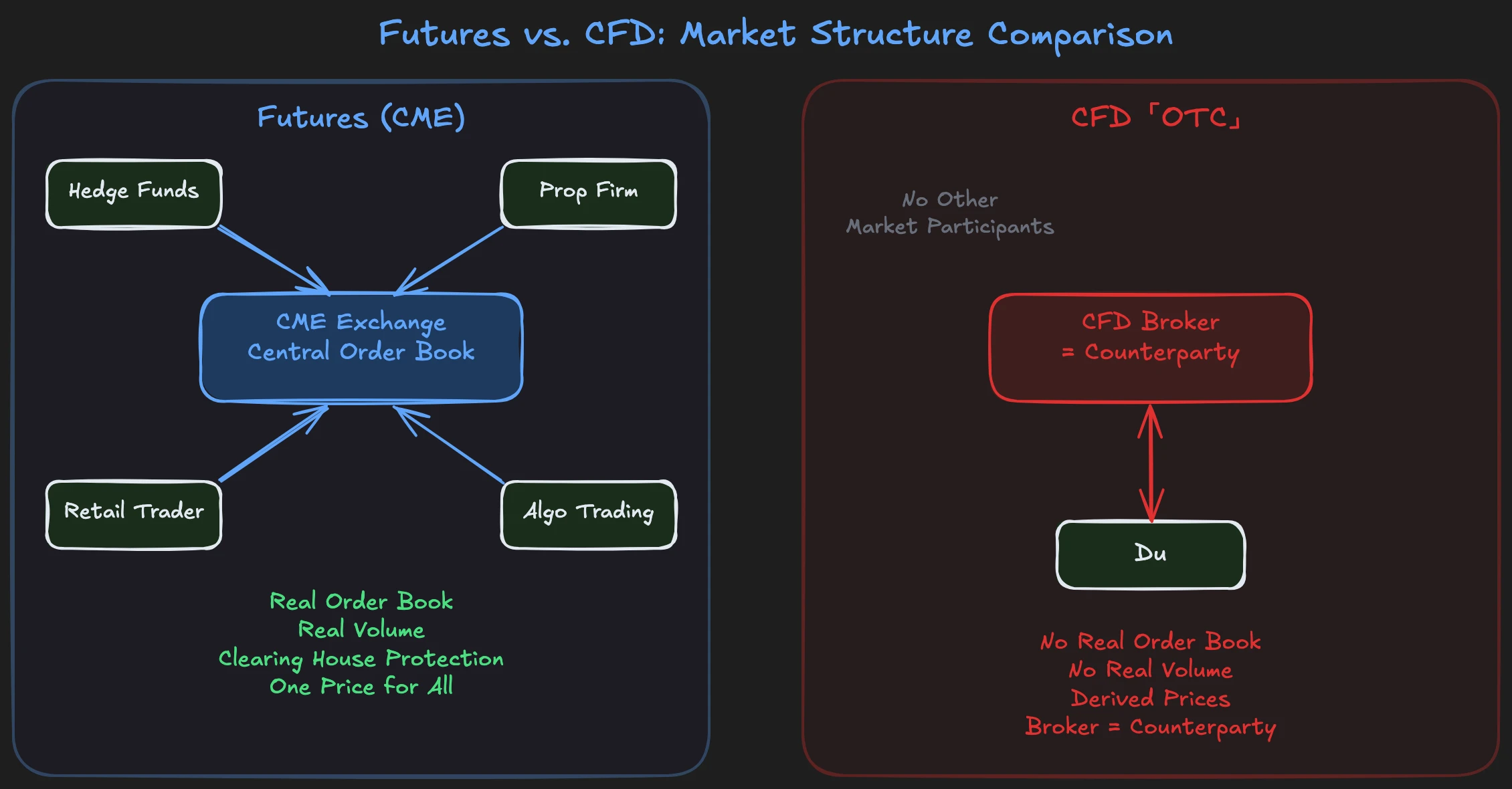

Futures offer real exchange transparency with centralized order book, real volume and clearinghouse protection. CFDs are OTC products where you trade against your broker as counterparty and only see derived prices without real market data. Anyone who wants to base their analysis on real transaction data cannot get around futures.

Most traders in Germany start with CFDs. This is due to availability, low entry barriers and CFD broker marketing. But CFDs have a fundamental problem that few understand: you don't trade at an exchange. You trade against your broker. A detailed comparison of both instruments can be found in our article Futures vs CFD.

With futures, it is different. Every futures contract trades on a centralized exchange. CME Group in Chicago is the world's largest futures exchange. No matter whether you sit in Germany, Japan or the USA: everyone goes through the same exchange. When the market moves a tick, every market participant worldwide sees it simultaneously. There is one price, one order book, one tape.

With CFDs, it doesn't work that way. Your CFD broker derives prices from the actual futures prices and provides you with their own prices. You don't see a real order book, real volume, real Time & Sales. You trade a copy. And the broker is your counterparty at the same time. This is not an accusation against CFD brokers; it is simply the structure of the product.

Why is this relevant? Because every serious order flow analysis is based on real exchange data. Footprint Charts, Volume Profile, Big Trades: all these tools need real transaction data from the exchange. They don't work with CFD data because the data only shows transactions between you and your broker, not the entire market.

There is also regulation. Futures are cleared through a clearinghouse. The exchange guarantees the fulfillment of every contract. With CFDs, your money depends on your broker's creditworthiness. These are different worlds.

Anyone who wants to trade order flow needs real exchange data. And real exchange data only comes through futures. A detailed overview of the best order flow software can be found in a separate article.

What a Future Actually Is

A future is a standardized contract to buy or sell a specific quantity of an underlying asset at a predetermined price on a specific date. The word "future" is the key. Futures are forward contracts. They have an expiration date.

Forward Contracts and Delivery

With index futures like the S&P 500 (ES) or Nasdaq-100 (NQ), there is no physical delivery. On expiration day, the difference between entry price and closing price is settled in cash. This is called Cash Settlement.

With commodity futures like Crude Oil (CL) or Gold (GC), it is different. There is actually physical delivery. If you hold an oil future until expiration, you are contractually obligated to take or deliver the corresponding quantity of oil. This is why commodity futures are taken very seriously in the institutional world: the delivery obligation is real. For retail traders, this is rarely a problem in practice because brokers automatically close positions before the Last Trading Day. But understanding the principle is important.

The Last Trading Day is the last day a futures contract can be traded. With the major index futures, it falls on the third Friday of the expiration quarter month (March, June, September, December). After that, the contract no longer exists. Anyone who has not closed or rolled their position beforehand is settled at the settlement price.

Front Month: Why Only the First Contract Matters

Futures contracts exist for several months simultaneously. You could theoretically trade the June contract, September contract or December contract. But in practice, almost everyone trades only the Front Month, i.e., the nearest expiring contract.

The reason is simple: the Front Month has the most open interest and the highest volume. This means the tightest spreads, fastest execution and least slippage. If you look at the various contract months on the CME website, you see the difference immediately: the Front Month trades enormous volumes while the later months are almost empty.

When the current Front Month approaches expiration, market participants switch to the next contract. This is called "rolling." The rollover typically happens a few days before the Last Trading Day. In this phase, you see volume moving from the old to the new Front Month.

The CME and the Product Universe

CME Group is the world's largest futures exchange and the central trading place for most futures you need as a trader. Actually, CME Group consists of four exchanges: CME itself (index futures like ES and NQ, currency futures), CBOT (treasury futures, agricultural commodities), NYMEX (energy like Crude Oil) and COMEX (metals like Gold). All four run on the Globex platform and are managed together.

Everything you need to know about a product can be found on cmegroup.com. No third party, no API copy: CME is the only source for contract specifications, trading hours and settlement prices.

The Most Important Products

For day traders, four index futures are most relevant:

- ES (E-mini S&P 500): The world's most traded index future. Tracks the S&P 500. High liquidity, tight spreads, clean market structure.

- NQ (E-mini Nasdaq-100): Tracks the Nasdaq-100. Significantly more volatile than the ES. Where the S&P makes 3 ticks, the Nasdaq makes 40. This opens additional trading opportunities but also higher risk.

- YM (E-mini Dow Jones): Tracks the Dow Jones Industrial Average. Less frequently actively traded.

- RTY (E-mini Russell 2000): Tracks the Russell 2000. Interesting for small-cap exposure, but less volume than ES or NQ.

In addition to index futures, there are commodity futures like CL (Crude Oil) and GC (Gold) as well as currency futures like 6E (Euro/USD). For European traders, the FDAX (DAX future) on Eurex is relevant, though with significantly less liquidity than US products.

In my trading, I focus primarily on ES and NQ. They have the best combination of liquidity, volatility and clear market structure.

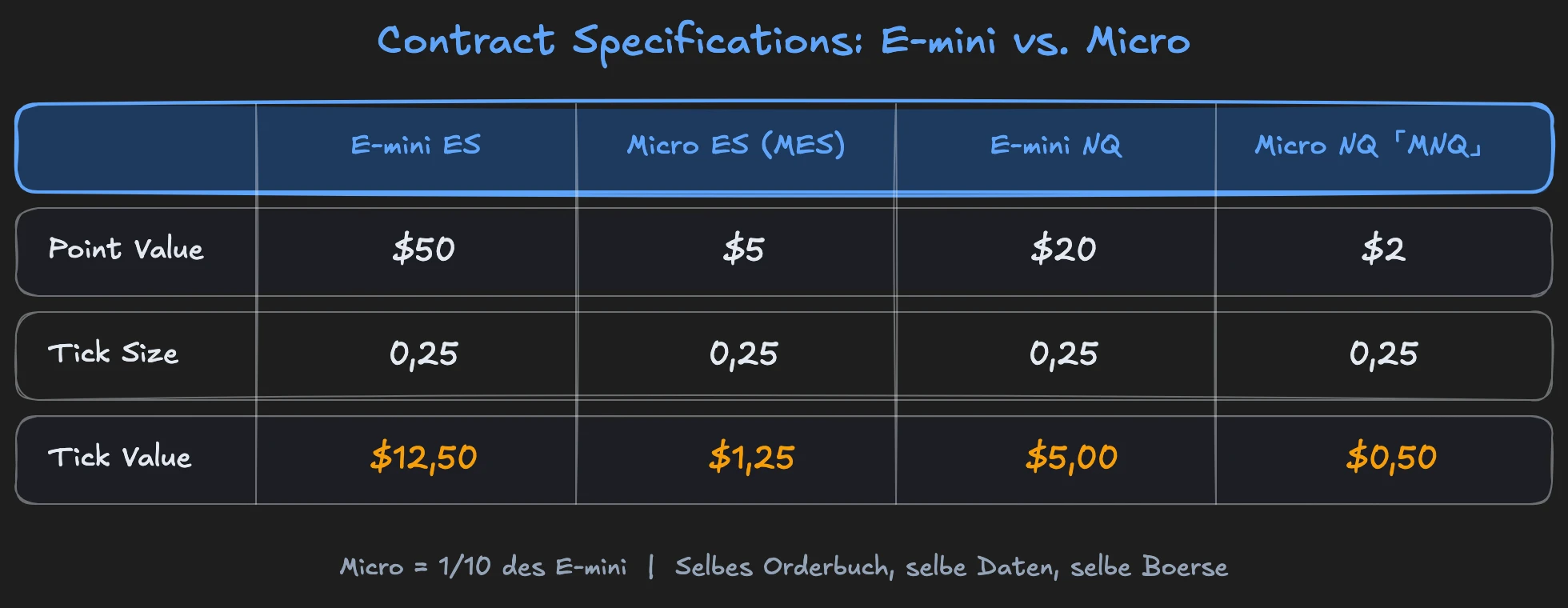

E-mini and Micro: Which Contract for Which Account

Since 2019, the CME has also offered Micro versions of the most important products. A Micro contract is exactly one-tenth the size of the corresponding E-mini:

| E-mini ES | Micro ES (MES) | E-mini NQ | Micro NQ (MNQ) | |

|---|---|---|---|---|

| Point value | $50 | $5 | $20 | $2 |

| Tick value | $12.50 | $1.25 | $5.00 | $0.50 |

| Tick size | 0.25 | 0.25 | 0.25 | 0.25 |

The critical point: Micro futures trade on the same exchange, with the same data and the same order book. You get the same transparency as the E-mini, only with one-tenth the exposure. Micros are ideal for getting started with futures trading. More on contract specifications, margin and position sizing for small accounts can be found in the guide Micro Futures Trading.

Contract Specifications You Must Understand

Every futures contract has exact specifications: point value, tick size, notional value and margin. Professional traders think in ticks, not points, because every tick is real money.

Points, Ticks and Notional Value

In ES, a point is the last place in the price, i.e., the ones digit. One point in ES has four ticks (0.25 per tick). The point value is $50, the tick value $12.50.

At an ES price of 5,000 points, the notional value of a single contract is $250,000 (5,000 x $50). That is the exposure you control with one contract. With two contracts, it is $500,000. This understanding is critical for your risk management.

In NQ, a point also has four ticks. The point value is $20, the tick value $5.00. Sounds like less, but NQ is significantly more volatile. In practice, NQ often moves multiples of ES in the same time span. The dollar movement per contract can therefore be similar or even higher.

An important difference from CFDs: with futures, you cannot trade half contracts. A contract is a contract. You cannot buy 0.5 ES. This makes position sizing more discrete than with CFDs, where you can trade arbitrarily small lots. But with Micro futures, you still have fine gradation.

Margin: Security Deposit, Not Credit

Many beginners confuse futures margin with credit. That is wrong. Margin with futures is a security deposit, a performance bond. The exchange holds this money to ensure you can cover your losses. You are not borrowing money. You are depositing collateral.

There are two types of margin:

- Initial Margin: The amount you must deposit to open a position. Set by the CME and changes regularly.

- Maintenance Margin: The minimum amount that must remain in your account as long as the position is open. If your account falls below this, you get a margin call.

For day traders, many brokers offer reduced intraday margins. A Micro NQ (MNQ) can be traded with a day trading margin of $50-100, while overnight margin is over $2,000. That is an enormous difference and the reason many traders trade exclusively intraday.

Trading Hours and Sessions

Futures trade almost around the clock. The CME Globex platform opens Sunday 5:00 PM (CT) and closes Friday 4:00 PM (CT), with a daily pause from 4:00 to 5:00 PM.

Not every session is equally relevant:

- Asian Session: Typically low volume in index futures. Little movement.

- European Session: Volume increases, first significant moves.

- US Cash Open (9:30 ET): This is when big money comes in. Most institutional orders are executed during the US session.

- Power Hour (15:00-16:00 ET): Closing session. Institutional portfolios are valued at the close. More volume is executed here than at any other time.

A risk many beginners underestimate: Circuit Breakers. In extreme volatility, the CME can temporarily halt trading (Limit Up / Limit Down). During a halt, you cannot open or close positions. If you are in a trade and the market is halted, you are stuck until trading resumes. This rarely happens with ES and NQ, but it does. Corona and surprising political events have shown this multiple times.

Order Types: What Really Moves the Market

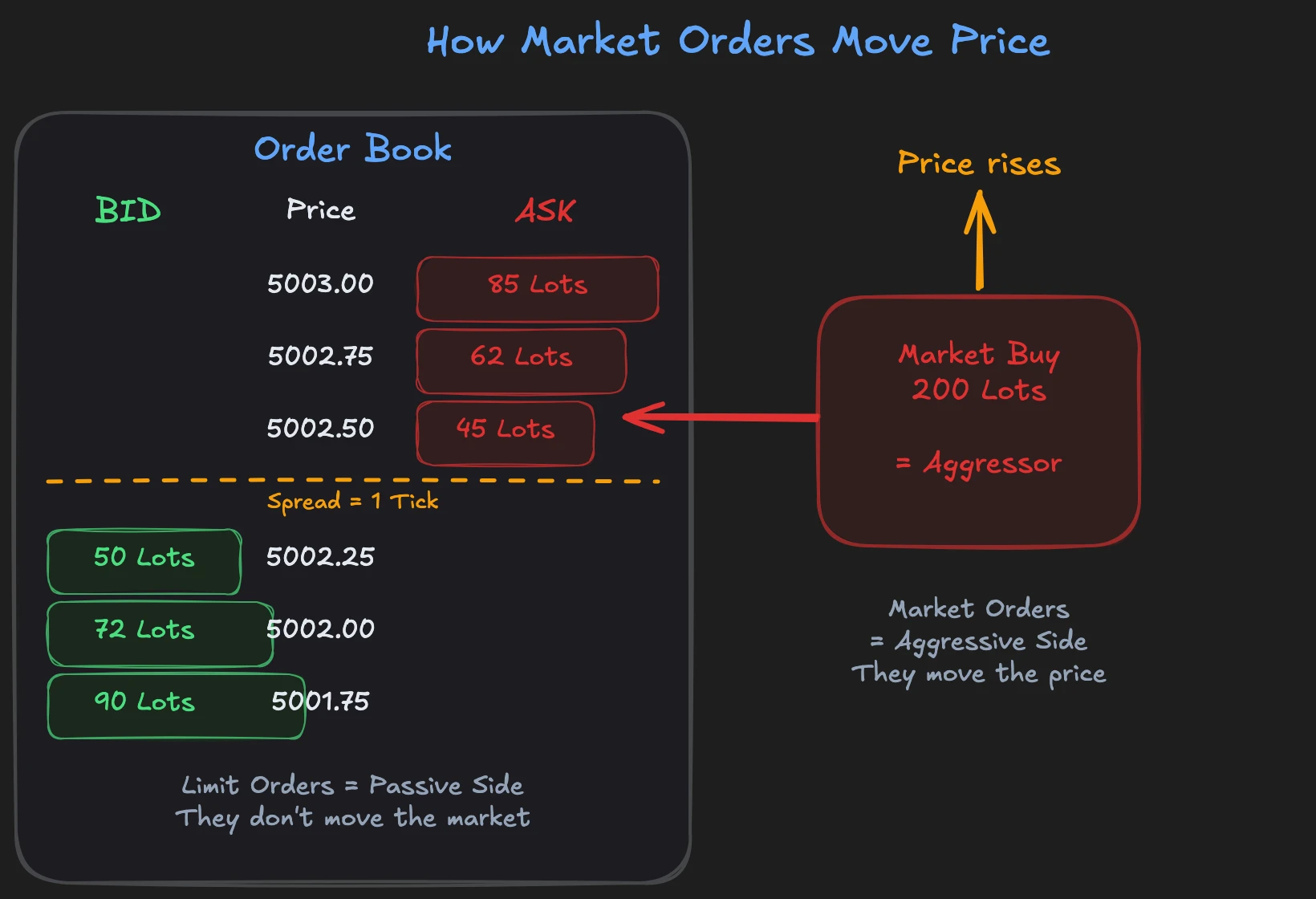

Most traders believe the market rises because there are "more buyers than sellers." That is wrong. With every single trade, there is exactly one buyer and one seller. Otherwise no trade happens. What moves the market is not the number of buyers or sellers, but the aggressiveness of the orders.

Market, Limit and Stop Orders

There are three basic order types, and each has a specific role:

Market Orders guarantee execution, but not the price. When you place a Market Buy order, you buy immediately at the best available Ask price. Price can move during execution. Market orders are always the aggressor. They hit the passive side in the order book and thereby move price.

Limit Orders guarantee the price, but not the execution. You set a price at which you want to buy or sell. Your order sits in the order book waiting for someone to hit you with a Market Order. Limit orders are passive. They don't move the market; they stand in its way.

Stop Orders are not Limit Orders, even if they look like one. A Stop Order is held with the broker and only triggers when price reaches a certain level. At that moment, it becomes a Market Order. Stop Orders are not visible in the order book. That is why we cannot see them directly in order flow, only their effect when they trigger. More on this in our article about Stop Runs.

Why Institutions Work with Limit Orders

This is where understanding the market really becomes important. The spread, i.e., the difference between Bid and Ask, is a cost factor with every trade. In ES, the spread is typically one tick: $12.50 per contract.

If you buy one contract with a Market Order, you pay $12.50 in spread. With 10 contracts, it is $125. With 100,000 contracts, which can be a normal daily volume for a large institution, it is $1,250,000. Per day. That is annual salaries lost to the spread.

That is why institutions trade most of their orders as Limit Orders. In my time as an institutional trader, that was the norm: we patiently waited for our price instead of aggressively crossing the market. The price guarantee of the Limit Order is more important to institutions than the execution guarantee of the Market Order.

This understanding is fundamental for reading Footprint Charts and Big Trades. If you see in the Footprint that massive volume is being absorbed on the limit side, you know: someone big is there who wants to buy or sell at this price and is willing to wait for it.

Who Trades Futures? The Five Market Participants

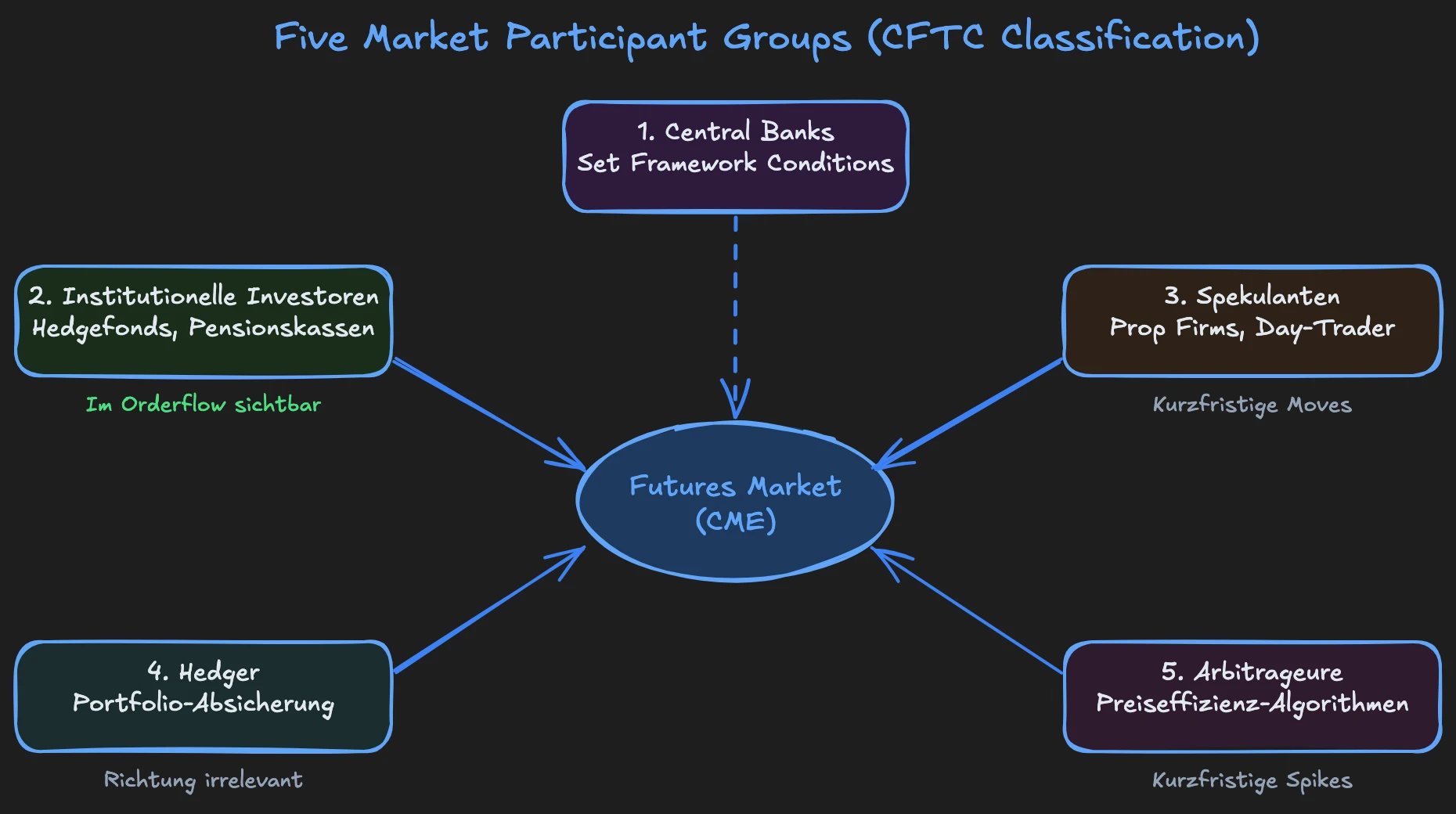

Various groups act in the futures market with different goals. The CFTC (Commodity Futures Trading Commission) publishes the weekly Commitments of Traders Report, which breaks down positions by trader type. Based on this classification, I distinguish five groups that you as a trader need to know. Each has different goals, timeframes and strategies. If you know who is on the opposite side of your trade, you understand why the market moves.

1. Central Banks: They move markets with words alone. An interest rate decision or Fed statement can move the NQ hundreds of points in seconds. Central banks rarely trade directly in the futures market, but their decisions set the framework for everyone else.

2. Large Investors (Institutional Investors): Hedge funds, pension funds, asset managers. This is the group you as a trader want to follow. They bring enormous capital and position themselves over days and weeks. Their activity is visible in order flow if you know what to look for.

3. Speculators: Proprietary trading firms, day traders, swing traders. This group reacts to short-term opportunities. They are particularly active in the scalping area. They can be relevant for short-term trades of 15-30 ticks.

4. Hedgers: Portfolio managers hedging their existing positions. A hedger with a large stock portfolio sells ES futures to limit their downside risk. They don't care about the direction of the futures market. They hedge. Following this group is pointless because their trades don't tell you anything about market direction.

5. Arbitrageurs: They are particularly important with index futures. When the ES future deviates from the actual S&P 500 index, arbitrage algorithms immediately strike. They buy the undervalued and sell the overvalued instrument until prices align again. This happens programmatically and in fractions of seconds. It explains the short, sharp price movements that immediately reverse and confuse many retail traders. You see a sudden spike of three ticks, and one second later price is exactly where it was before. That was no mysterious manipulation. That was an arbitrageur snapping price back to fair value.

One point I keep emphasizing: institutions have no magic button. They have to trade with Bid and Ask just like everyone else. Their orders are visible in the order book and tape. The difference is the size, speed and systematic approach. But the mechanics are the same.

How to Start with Futures Trading

Entering futures trading requires three things: a broker with real exchange access, a real-time data feed, and the right risk understanding. Here is the pragmatic path.

1. Choose a broker: You need a broker that gives you direct access to the CME, not a CFD broker that replicates futures prices. Well-known futures brokers are AMP Futures, NinjaTrader and Interactive Brokers. Commissions are low (often under $1 per Micro contract per side). A complete comparison with costs, platforms and data feeds can be found in the Futures Broker Comparison for Germany.

2. Real-time data feed: For futures, you need a real-time data feed from the exchange. This costs $10-15 per month depending on the provider. Without this feed, you see delayed data, which is worthless for active trading.

3. Simulated trading: Every reputable futures broker offers a demo account with real market data. Use it. Trade in the simulator for at least a few weeks before risking real money. In the simulator, you learn the platform, order execution and market speed without losing money.

4. Start with Micro Futures: MES and MNQ are made for getting started. One tick in MNQ is $0.50. This gives you the ability to gain real experience without a normal losing day destroying your account.

5. Understand position sizing before live trading: Before you make your first real trade, you need to know how much you risk per trade. Not in percentage, but in dollars. If your stop is 10 ticks away and you trade one MNQ contract, you risk $5. With an MES contract, it would be $12.50. Calculate this for each product before going live.

Regulation and Margin Calls: What German Traders Need to Know

When trading futures on the CME from Germany, there are some regulatory things you should understand. I regularly get questions about this, and the answers surprise most people.

BaFin and US Futures

BaFin regulates German financial service providers, but has no jurisdiction over US futures exchanges or US brokers. If you open an account with a US broker like AMP Futures or NinjaTrader, that account falls under the supervision of the CFTC and NFA in the USA, not BaFin. This is neither illegal nor problematic. As a German citizen, you can easily maintain an account with a US broker and trade futures. You must, of course, tax the profits in Germany.

Margin Calls: The Big Difference from CFDs

Since 2018, the EU has had Negative Balance Protection for CFDs (introduced through ESMA product intervention). This means: your CFD account cannot go below zero. The broker must close your positions first. This sounds good, but there is a catch: it only works because the broker is your counterparty and sets the rules.

With US futures, there is no such protection. Your account can theoretically go negative, and you are obligated to cover the shortfall. This is the so-called margin call. In practice, this happens extremely rarely because brokers issue margin calls and liquidate positions before it comes to that. But in a flash crash or overnight gap over the weekend, it is possible. That is why I always say: only trade with money you can afford to lose, and don't hold positions overnight if you are not consciously taking the risk.

Which Brokers Work for German Traders?

The broker landscape for German futures traders looks like this:

- AMP Futures and NinjaTrader: US brokers with direct CME access. Low commissions, good platforms. No BaFin protection, but CFTC/NFA regulated. Accounts are held in the USA.

- Interactive Brokers: Has both a US and EU entity (through Ireland/Hungary). You can trade through the EU entity and then have some European regulation, though Negative Balance Protection still doesn't apply to futures.

- LYNX and CapTrader: German resellers of Interactive Brokers. BaFin-registered, German-language support. However, orders still go through Interactive Brokers. Somewhat higher commissions than directly with IB.

Which broker is right for you depends on your capital, platform requirements and comfort with English-language support. A detailed comparison with costs, data feeds and platforms can be found in the Futures Broker Comparison for Germany.

FAQ: Futures Trading

How much capital do I need for futures trading?

Theoretically, you can start with $500-1,000 if you trade Micro Futures exclusively intraday. Realistically, I recommend $3,000-5,000 for Micro Futures. This gives you enough buffer for a losing streak without falling below maintenance margin and having positions forcibly liquidated.

Are futures more dangerous than stocks or CFDs?

Futures are leveraged, yes. But the leverage is transparent and controllable. You know exactly how much a tick costs, what the notional value is and how much margin you need. With CFDs, you are offered "30:1 leverage" without seeing the notional value or real exposure calculation. Futures are not more dangerous; they are more honest. The risk lies not in the instrument, but in position size.

Do I need special software for futures trading?

For pure price analysis, TradingView is sufficient. For order flow analysis, you need specialized software like ATAS or Bookmap that can visualize real-time exchange data. Costs range from $50-200 monthly for software and data combined. A detailed overview can be found in our Order Flow Software Comparison.

Can I start directly with futures or should I trade CFDs first?

Start directly with futures. Micro Futures are made exactly for that. A detour through CFDs brings you bad habits (no real order book, artificial prices) and costs you time. Start with MES or MNQ in the simulator, then switch to a small live account and learn from the beginning with real data.

Learn Futures Trading: The Next Step

Futures are the foundation for professional trading. With a real order book, real volume and the transparency of a centralized exchange, you have access to the same data as institutional market participants. No other instrument gives you that.

In our mentoring program, you'll learn these concepts in over 1,500 video lessons with real chart examples. The Trader Framework course dedicates 22 lessons to the fundamentals alone, from contract understanding to order types. The Bootcamp then goes directly into practice with Footprint Charts and Volume Profiles.