News Trading: How to Trade News Events and Economic Releases Profitably

News trading is the practice of taking positions in financial markets based on the release of economic data, geopolitical developments, or corporate earnings. A sound news trading strategy does not predict the news itself but instead focuses on managing the reaction, the volatility, and the opportunity that follows. Most traders lose money on news events not because they lack information, but because they lack a framework.

Risk Disclaimer: Trading futures and other financial instruments involves significant risk of loss. Past results are not indicative of future performance. Only trade with capital you can afford to lose.

I have traded through hundreds of major events, from surprise tariff announcements to FOMC rate decisions. The lesson I took away from my institutional time is simple: the event itself is noise. The market's reaction is signal. Everything in this article is built around that distinction.

The Three Categories of News Events

Not all news is created equal. The first step in any event-driven trading framework is understanding what kind of event you are dealing with, because each category demands a different playbook.

Category 1: Scheduled Macro Releases

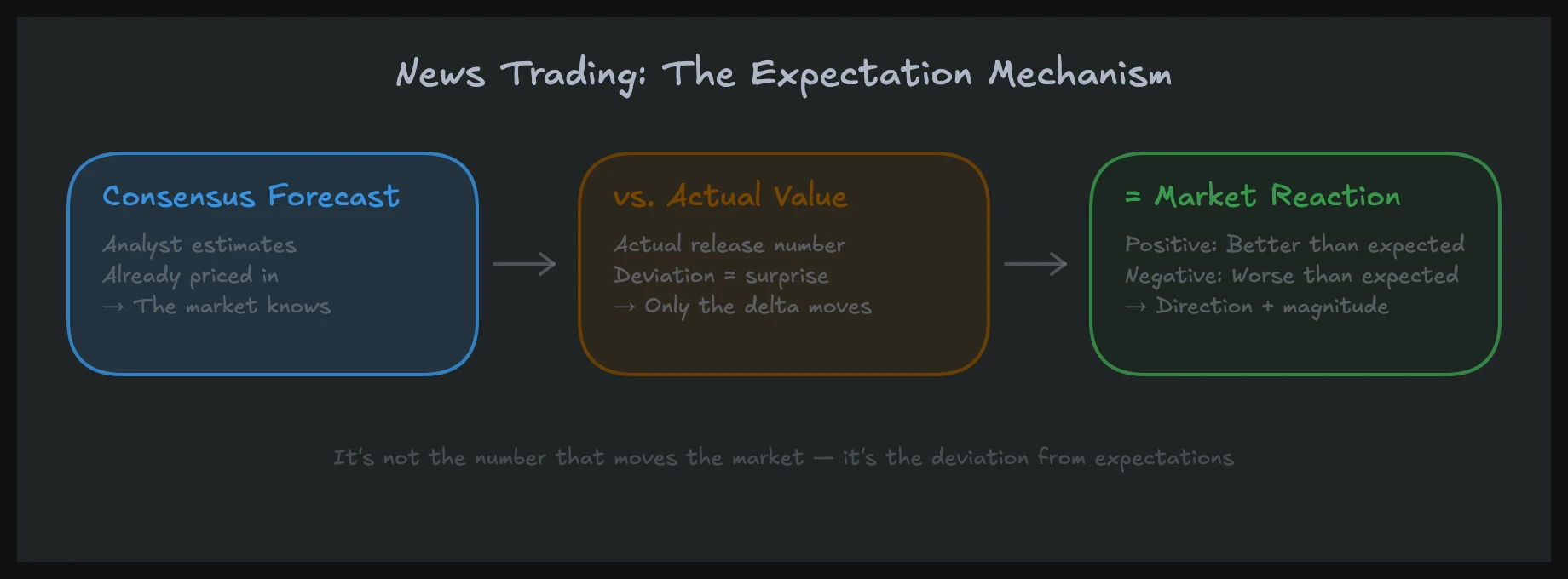

These are the events you can prepare for. CPI, NFP, FOMC decisions, GDP prints, ISM data. They appear on the economic calendar weeks in advance, have published consensus forecasts, and follow a predictable rhythm. You know the date, the time, and roughly what the market expects.

The key variable is the deviation from consensus. A CPI print of 3.2% when the market expects 3.2% barely moves the needle. The same 3.2% when expectations sit at 2.9% creates a repricing event across bonds, equities, and currencies simultaneously. For a deeper look at how these macro numbers flow through the system, see the guide on macroeconomics for traders.

Scheduled events are where preparation gives you the largest edge. You know they are coming. You can plan your position sizing, your stop placement, and your approach in advance. There is no excuse for being caught off guard by NFP when it happens the same Friday every month.

| Feature | Scheduled Macro | Unscheduled Geopolitical | Earnings |

|---|---|---|---|

| Timing | Known (calendar) | Unknown | Known (season) |

| Consensus available | Yes | No | Yes (EPS estimates) |

| Instruments affected | Broad (indices, bonds, FX) | Sector-specific or broad | Single stock, sometimes sector |

| Typical NQ move | 50-200 points | 100-500+ points | Indirect, through sector rotation |

| Preparation possible | High | Low | Medium |

| Best approach for most traders | Sit out or secondary move | Reduce exposure, wait | Trade the reaction, not the guess |

Category 2: Unscheduled Geopolitical Events

Tariff announcements, military conflicts, sanctions, political crises. These hit without warning and create the kind of volatility that destroys unprepared accounts. The Trump tariff announcements in 2025-2026 are a textbook example: a single social media post moved NQ 300+ points in minutes, with no consensus forecast and no preparation window.

Geopolitical events are different from macro releases in one fundamental way: there is no consensus to deviate from. The market is not pricing a specific outcome and then adjusting. It is reacting to entirely new information, often with incomplete details and conflicting reports. This is the domain of black swan events, where fat-tail risk becomes real.

When I traded at a prop desk, our rule for unscheduled geopolitical events was straightforward: cut exposure immediately, ask questions later. The traders who tried to be heroes during the initial chaos were the ones who blew up. The traders who survived reduced their size, waited for clarity, and then acted on the secondary move.

Category 3: Earnings Releases

Earnings season creates event risk concentrated in individual names, but the effects ripple into index futures through sector rotation and sentiment shifts. A bad NVIDIA print doesn't just move NVDA; it reprices the entire semiconductor sector and drags NQ with it.

For futures traders, earnings matter most when mega-cap names report. AAPL, MSFT, NVDA, AMZN, GOOGL, and META collectively represent such a large portion of the Nasdaq-100 that their individual earnings can move NQ 50-100 points in the after-hours session.

The preparation framework is similar to scheduled macro: know when the report drops, know consensus EPS and revenue expectations, and have a plan for both beats and misses. But the execution window is different because most earnings hit after the cash close, meaning your primary tool is the overnight futures session with thinner liquidity.

The Three Approaches to Any News Event

This framework comes from how I was trained on the institutional side, and I have applied it to every type of event for over a decade. Whether it is CPI, a tariff headline, or an NVDA earnings surprise, the same three approaches apply. I detailed this framework specifically for Non-Farm Payrolls in the NFP trading strategy article, but it generalizes to any event.

Approach A: Sit Out (Recommended for Most Traders)

No trade, no risk. This is not cowardice; this is discipline. If you do not have a tested, repeatable edge specifically for event volatility, sitting out is the highest expected-value decision you can make.

Sitting out does not mean ignoring the event. You still watch, take screenshots, note the reaction, study how price moves through the order book. You build the pattern recognition that eventually allows you to trade events profitably, but you do it without putting capital at risk during the learning phase.

In my experience, 80% of retail traders who actively trade news events would have better annual returns if they simply went flat 30 minutes before every scheduled release and waited an hour after. That is not a guess. I have reviewed hundreds of trading journals through our coaching program, and the pattern is overwhelmingly clear: event-day losses eat into weeks of good trading.

The risk management principle here is simple. Your edge exists in normal market conditions. News events temporarily destroy normal conditions. Why would you trade in an environment where your edge does not apply?

Approach B: Fade the Initial Spike (Experienced Traders Only)

The first reaction to any news event almost always overshoots. NQ drops 150 points on a hot CPI print and recovers 100 within 20 minutes. ES spikes 80 points on a dovish FOMC statement and gives back 50. This pattern exists because the initial move is driven by algorithmic market makers pulling liquidity, stop cascades, and emotional retail orders, not by reasoned repositioning.

The fade setup requires patience and order flow confirmation:

- Wait 5-15 minutes after the release. Never fade the initial move in real time.

- Watch for exhaustion in the aggressive side. If sellers drove the spike down, look for selling to dry up in the Footprint chart.

- Enter only when you see the opposing side step in with size. Real bids appearing, not just covering.

- Use a tight stop beyond the spike extreme. If wrong, you are out quickly.

- Target 40-60% of the spike range. Do not expect a full reversal.

The danger: sometimes the spike is not a spike. Sometimes it is the beginning of a sustained trend move. A CPI print that genuinely changes the Fed's rate path will not fade. A tariff announcement that restructures global trade will not fade. You must have the experience to distinguish between an emotional overreaction and a genuine repricing event. If you cannot make that distinction quickly, use Approach A.

Approach C: Trade the Secondary Move (Best Risk/Reward)

Wait 30-60 minutes after the event. Let the initial chaos play out. Spreads normalize, emotional traders are flushed, and the market begins to show its true hand.

After 30 minutes, you have real information:

- Has the market accepted the new price level, or is it rejecting back toward the pre-event range?

- Where is real volume trading? The Volume Profile after the event tells you where institutions are actually positioning, not just where the stop runs went.

- Is VWAP holding above or below the pre-event level? This gives you directional bias.

- What is /ZN doing? Bond market confirmation (or divergence) tells you whether the equity reaction is likely to sustain.

This approach has the highest success rate because you are trading with information instead of speculation. You have already seen how the market digested the news. You are not guessing; you are reading.

The trade-off is that you miss the initial move entirely. That is acceptable. The initial move is high variance and low reliability. The secondary move is lower magnitude but far more tradeable.

Why Algo Scanning Creates False Moves in 2026

In 2026, the news trading landscape looks fundamentally different from even two years ago. Algorithmic systems now scan news headlines, social media posts, and even audio feeds in milliseconds. When a CPI number hits, algos react before you can blink. When a tariff headline drops on social media, keyword-scanning bots move the market before human traders have finished reading the sentence.

This creates a specific problem: false moves. Algos react to keywords, not context. "Tariff increase" triggers selling regardless of whether the tariff applies to a $500 million niche product or a $200 billion trade category. "Inflation higher than expected" triggers a bond sell-off even when the overshoot is 0.1% and entirely driven by a seasonal adjustment quirk.

I have seen NQ drop 80 points on a headline that, upon closer reading, was a restatement of existing policy. The algos parsed "tariff" and "increase" and sold. Human traders who read the full context knew it was a non-event. The market recovered within 15 minutes.

This is actually good news for patient, informed traders. The algo-driven false moves create opportunities for those who can read context. Your human advantage in 2026 is not speed. You will never be faster than a co-located server. Your advantage is understanding. You can read a full statement, assess the actual economic impact, compare it to what is already priced in, and act on the secondary move with conviction while the algos are already done with their keyword-triggered positioning.

The VIX and volatility framework helps here. When VIX is elevated, algo-driven false moves are amplified because liquidity is thinner. When VIX is low, the same headlines produce smaller reactions. Knowing the volatility regime tells you how aggressively to size your secondary move trades.

Building Your Event Preparation Checklist

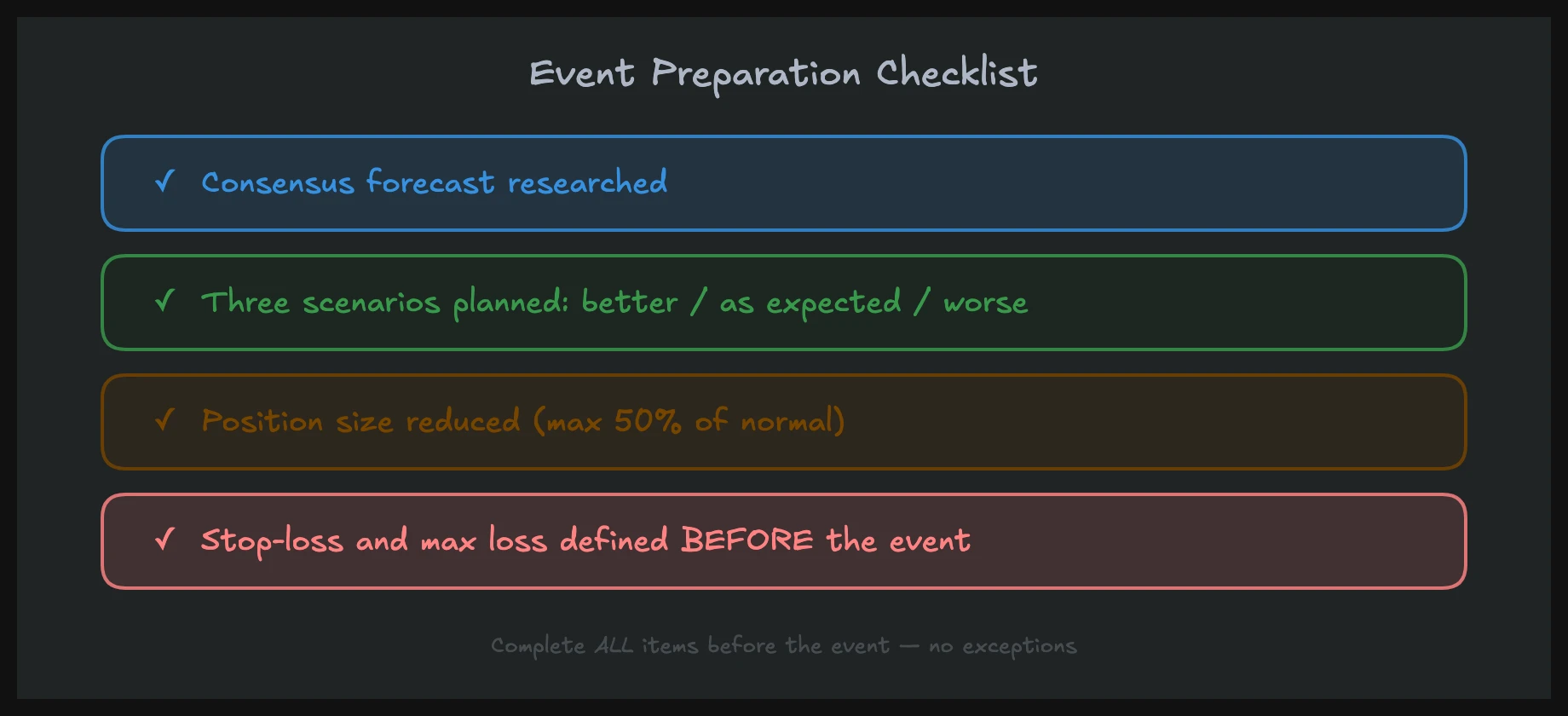

Professional event trading is not about reacting. It is about preparing. Here is the checklist I use before every scheduled macro release:

The evening before:

- Check the economic calendar for the exact release time, consensus forecast, and any related data points releasing simultaneously.

- Review current market positioning. Where is NQ relative to its recent range? Is the market already leaning in one direction (pricing in a beat or miss)?

- Check /ZN (10-year Treasury futures). Bond market positioning before macro data gives you a clue about how rates-sensitive the equity reaction will be.

- Set alerts, not orders. I want to be notified when the data drops, but I do not want resting orders that might get filled at terrible prices during the initial spread widening.

30 minutes before the release:

- Flatten any positions you do not want to hold through the event. This is non-negotiable.

- Reduce your maximum position size for the post-event window. Half size is a good starting point.

- Note the current ES/NQ level, VWAP, and the day's Value Area. These become your reference points for the post-event reaction.

At the release:

- Watch, do not trade. Note the initial direction, the magnitude, and how quickly the move happens.

- Check the actual numbers against consensus. What is the deviation? Is it a meaningful surprise or noise?

15-30 minutes after:

- Assess: is the initial move holding, extending, or fading?

- Check order flow: is there follow-through from institutional-sized orders, or is the move running on thin volume?

- If using Approach C, begin looking for entry setups in the direction of the accepted move.

For unscheduled geopolitical events, the checklist is shorter: reduce exposure immediately, wait for clarity, then apply the secondary move framework once you understand what actually happened.

Common Mistakes in News Trading

Holding positions through events without adjustment. This is not trading; it is gambling with extra steps. If you hold a full-size NQ long through CPI with a 20-point stop, you are effectively hoping that CPI comes in soft. Hope is not a strategy.

Trading the headline instead of the reaction. "CPI came in hot, so I shorted NQ." That sounds logical but ignores that the market may have already priced in a hot print. If consensus was 3.0% and whisper numbers were 3.3%, a 3.2% print is actually dovish relative to what the fast money expected. You must trade the reaction, not the headline.

Ignoring the bond market. Macro data moves bonds first, equities second. If CPI surprises to the upside and /ZN barely moves, the equity selloff is unlikely to sustain. If /ZN drops hard, the equity impact is real. Always check the rates reaction. The relationship between interest rates, bonds, and equities is the foundation of event trading.

Revenge trading after a stop-out. You shorted the fade at minute 5, got stopped out, and now you are angry and want to "make it back." This is the single most destructive pattern I see on event days. One bad trade becomes three. Three become five. The daily loss goes from manageable to account-threatening. Set a maximum loss for event days and respect it.

Overtighting stops during high volatility. Normal 10-point stops on NQ do not work when the instrument is moving 50 points in a minute. Either widen your stops and reduce your size, or do not trade at all. A tight stop in a high-volatility environment is just a guaranteed loss with extra friction.

The Role of Position Sizing on Event Days

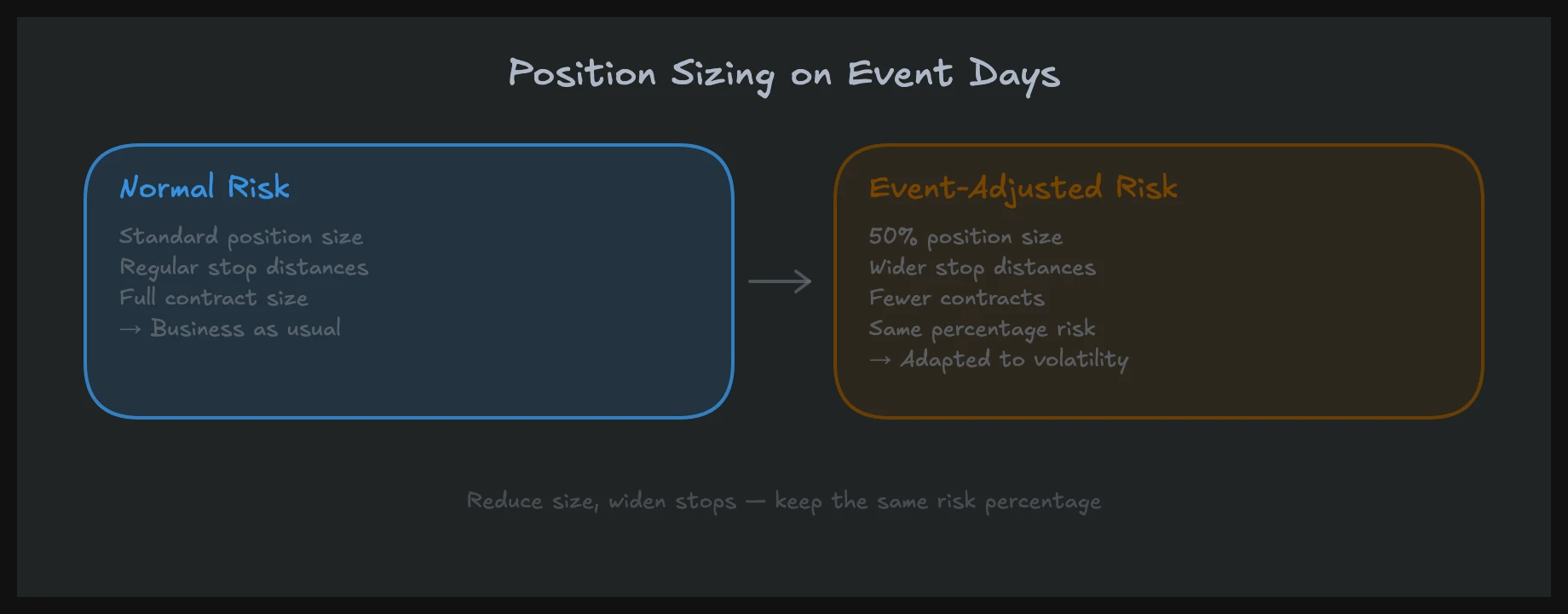

This deserves its own section because it is where most traders fail. Your normal position sizing does not apply during news events. Period.

If your standard NQ trade is 4 contracts with a 15-point stop (risk: $1,200), that same 4-contract position with a 60-point event-driven move against you represents $4,800 in risk, four times your normal exposure. The math does not work.

On event days, I reduce to 1-2 contracts maximum, regardless of my conviction. The lower size allows for wider stops that accommodate event volatility without exceeding my daily risk limit. It also removes the emotional pressure that leads to impulsive decisions.

The rule from our Money Management curriculum applies directly here: when uncertainty peaks, exposure decreases. That is not optional. It is the difference between surviving a bad event day and blowing your monthly P&L.

For a complete framework on sizing and risk control, see the risk management guide.

Putting It All Together: A Framework for Every Event

The beauty of this framework is its simplicity. Three categories of events, three approaches for trading them, and a preparation checklist that works across all of them.

For scheduled macro events (CPI, NFP, FOMC): prepare the evening before, go flat before the release, and either sit out entirely or trade the secondary move after 30-60 minutes. The NFP trading strategy article walks through this in detail for the most volatile regular release on the calendar.

For unscheduled geopolitical events (tariffs, conflicts, sanctions): reduce exposure immediately, do not try to interpret the headline in real time, and wait for the secondary move once the actual impact becomes clear. Review the Trump tariffs case study and black swan events for real examples of how these play out.

For earnings: know when mega-cap names report, understand the consensus, and be prepared for overnight NQ volatility. Trade the next-day reaction, not the after-hours spike.

In all cases, the human advantage is the same: patience. Algos will always be faster. They will never be more patient or more contextual. That is your edge.

In our macroeconomics course with 20 video lessons, you'll learn how bonds, interest rates, and economic data interact, and how to prepare for events systematically. At united-daytraders.com, you'll find over 1,500 video lessons from institutional traders.

FAQ

Should I trade before news releases?

For scheduled macro releases like CPI, NFP, or FOMC, no. The risk/reward is extremely unfavorable because you are essentially betting on the number, which is a coin flip at best. Professional traders go flat before major releases and trade the reaction afterward. The only exception is if you have a defined position with stops wide enough to absorb the event volatility and you have already accounted for that risk in your daily plan. For 95% of traders, flat is the right answer.

How do I protect myself from unexpected news?

You cannot predict geopolitical shocks, but you can prepare for them structurally. First, never risk more than 1-2% of your account on any single trade, so a surprise move cannot destroy you. Second, always have stops in the market, even if they are wider than normal. Third, reduce overall exposure during periods of elevated geopolitical tension (election seasons, trade negotiation windows, military escalations). Check the VIX daily. When it is rising, the market is telling you that uncertainty is increasing.

Which news events move the NQ the most?

In order of average impact: FOMC rate decisions (especially when accompanied by updated dot plots), CPI and Core CPI, Non-Farm Payrolls, unscheduled tariff or trade policy announcements, and mega-cap tech earnings (NVDA, AAPL, MSFT). FOMC days routinely produce 150-300 point NQ ranges. CPI days average 100-200 points. NFP days typically see 80-150 points of range expansion. But the magnitude depends entirely on the deviation from consensus, not the event itself.

Is news trading suitable for beginners?

No. News trading requires experience with volatile conditions, fast decision-making, and the emotional discipline to sit on your hands when every instinct tells you to act. Beginners should spend their first 6-12 months going flat before every scheduled event and studying the reactions afterward. Build your pattern recognition without risking capital. Once you can consistently identify whether an initial move is likely to fade or sustain, based on order flow and volume profile analysis, you can begin with Approach C (secondary moves) at reduced size.

How long should I wait after a news event before trading?

For scheduled macro releases, 30-60 minutes is the standard window. This allows spreads to normalize, the initial stop runs to complete, and real institutional flow to become visible. For unscheduled geopolitical events, the wait can be longer, sometimes several hours, because the full scope of the event may not be clear immediately. The key signal is not time itself but whether the market has established a new accepted range. When Volume Profile shows a clear new Value Area forming, the dust has settled enough to trade.