Trading Loss Offset Rules in Germany: 2025 Changes Explained

Loss offset in trading is the targeted tax offset of trading losses with profits within legally defined offset pots. Since the Annual Tax Act 2024, significantly better rules apply for futures traders. This article shows you the two pots, loss carryforward, loss certificate, and strategies with which you legally reduce your tax burden.

Tax Disclaimer: This article is for general information purposes only and does not replace individual tax advice. Tax regulations can change and depend on personal circumstances. Always consult a qualified tax advisor before making tax decisions.

The Two Loss Offset Pots

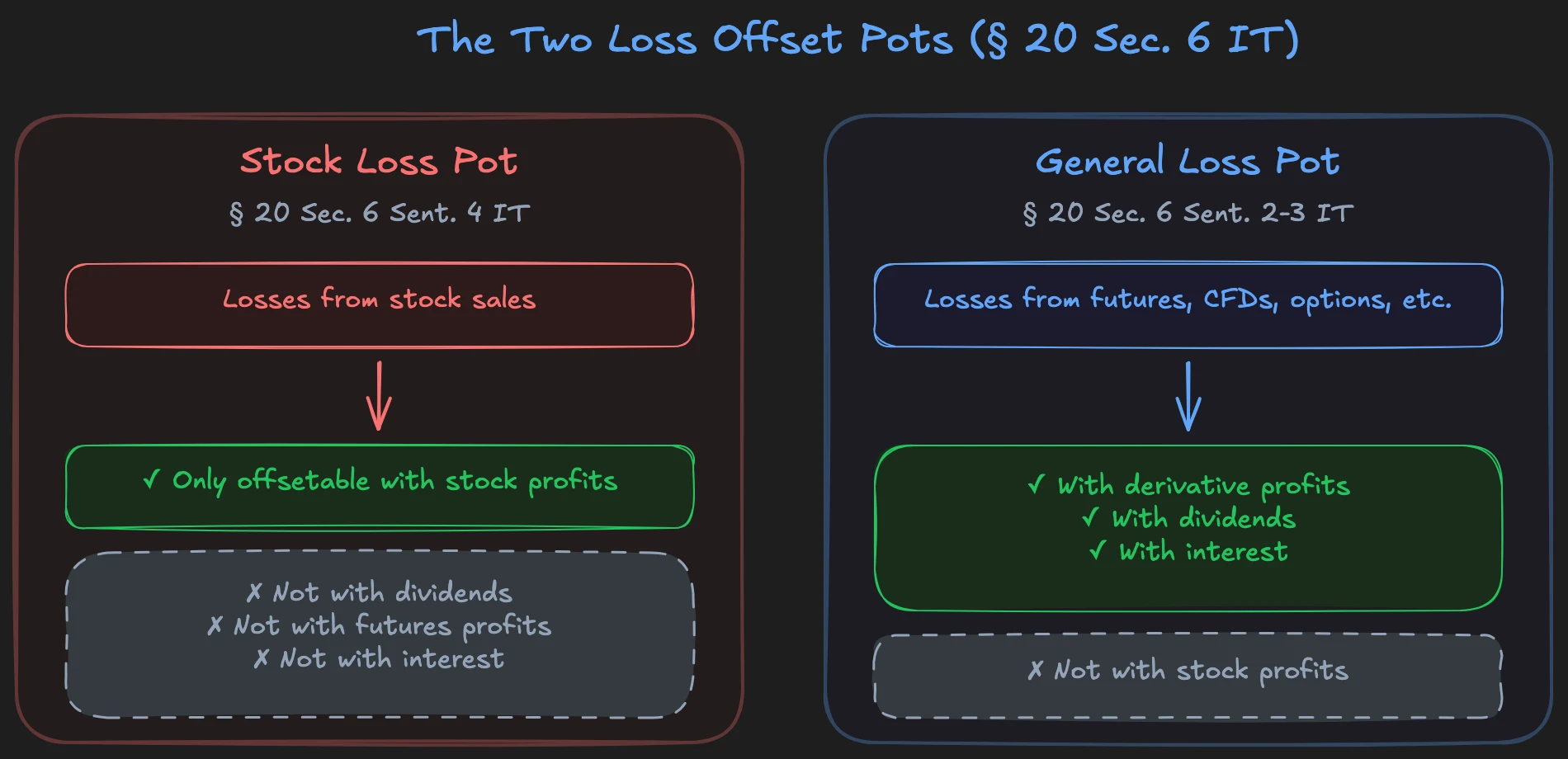

German tax law separates losses from capital income into two pots under § 20 Abs. 6 EStG. Understanding this separation is the foundation for any tax optimization.

Stock Loss Pot: Losses from the sale of stocks can only be offset with profits from the sale of stocks (§ 20 Abs. 6 Satz 4 EStG). Not with dividends, not with futures profits, not with interest. Only stock profits. As long as you don't realize stock profits, the losses remain in the pot and are carried forward.

General Loss Pot: Losses from futures, CFDs, options, certificates, and all other derivatives can be offset with each other. Additionally, they can be offset against dividends, interest, and other capital income. Only not against stock profits.

In our Tax module at United Daytraders, I cover the offset pots in a dedicated lesson because I know from personal experience how much money traders leave on the table here.

A Concrete Example

Let's take a typical case: In one year, you achieved 15,000 euros profit from NQ futures, 8,000 euros loss from ES futures, and additionally 3,000 euros loss from stock sales.

The futures offset runs in the general pot: 15,000 euros profit minus 8,000 euros loss equals 7,000 euros taxable profit. On this you pay 26.375% withholding tax (25% withholding tax plus 5.5% solidarity surcharge, without church tax), so approximately 1,846 euros.

The 3,000 euros stock loss? That stays in the stock loss pot. It can't be offset with your futures profits. So you have 4,000 euros actual net profit (7,000 minus 3,000), but pay 1,846 euros taxes on 7,000 euros. The stock losses are carried forward and wait for future stock profits.

For active futures and CFD traders, this is good news: Most losses land in the general pot and can be fully offset there with profits from other derivatives. Only those who also trade stocks need to keep the pot separation in mind.

You can find all tax rules for traders in our article on trading taxes in Germany.

The 20,000 Euro Cap: What Changed

From 2021, a regulation applied that massively disadvantaged futures traders. § 20 Abs. 6 Satz 5 EStG (introduced by the Annual Tax Act 2020) limited the offset of derivatives losses to 20,000 euros per year. Anything above that was carried forward, but in the following year also only credited up to 20,000 euros.

What this meant in practice is shown by an example: A trader realized 60,000 euros futures profit and 50,000 euros futures loss. His actual net profit was 10,000 euros. Under the old rule, however, he could only credit 20,000 euros of his losses. So 40,000 euros was taxable. The withholding tax on that: around 10,550 euros. On an actual net profit of 10,000 euros. More tax than profit.

The Annual Tax Act 2024 (published on December 5, 2024 in the Federal Law Gazette) completely abolished this cap. The new regulation applies retroactively in all still-open cases (§ 52 Abs. 28 EStG). Losses from derivatives can now again be fully offset with corresponding profits. Those who had switched to CFDs because of the cap can now trade futures again without tax disadvantage.

The BFH case VIII R 11/24, which was to clarify the constitutionality of the cap, was decided on March 28, 2025 in favor of the plaintiffs. The BFH found that the plaintiffs would have prevailed on the merits and imposed the procedural costs on the tax office. Those who had high derivatives losses in the years 2021 to 2024 and kept the tax assessments open can claim the abolition retroactively. Discuss this with your tax advisor.

Loss Carryforward and Loss Certificate

Loss Carryforward: Losses Don't Disappear

Unoffset losses are automatically carried forward to the next year. This loss carryforward is unlimited in time and amount (§ 20 Abs. 6 Satz 2 and 3 EStG). Whether you couldn't offset 500 euros or 50,000 euros, whether it takes one year or ten: The losses are preserved and offset as soon as you realize corresponding profits.

With a German broker, this works automatically. Your broker maintains the loss offset pots internally and automatically offsets losses from the previous year with new profits. You don't have to do anything.

Loss Certificate: When You Have Multiple Brokers

It gets more difficult with multiple brokers. Broker A doesn't know your losses at Broker B. If you want to offset losses across brokers, you need a loss certificate under § 43a Abs. 3 Satz 4 EStG. Here's how it works:

- Check: Identify which losses lie with which broker in which pot.

- Request: Request the loss certificate from your broker before December 15 of the current year. This is a hard deadline, not a guideline. The request is irrevocable.

- Pot is closed: The broker sets the loss pot for the relevant year to zero and issues you the certificate.

- Tax return: Submit the certificate together with Annex KAP with your tax return.

- Offset: The tax office offsets the losses across brokers.

Important: As soon as you request the loss certificate, the loss pot is reset at that broker. The losses can no longer be automatically carried forward there. You then have to run the offset through the tax return.

"Those who only use one broker don't need a loss certificate. Everything runs automatically there. It only gets complicated with multiple accounts, and then the December deadline is the date you can't miss."

For traders with foreign brokers: You do the entire loss offset yourself via Annex KAP anyway. The loss certificate is only relevant here if you simultaneously have a German broker and want to include losses from there in the tax return.

Tax-Loss Harvesting: Targeted Loss Realization

Tax-loss harvesting means: You consciously sell positions with unrealized losses before year-end to reduce realized profits for tax purposes. In Germany, there's no wash-sale rule like in the US. You can sell a position, realize the loss, and then reopen the position. However, tax authorities could examine an abuse of structuring under § 42 AO in cases of obvious back-and-forth trading.

When It's Worthwhile

You have high realized profits in the current year and simultaneously open positions with unrealized losses in the same pot. Example: You have 12,000 euros realized futures profits and hold a position with 4,000 euros unrealized losses. If you close the position before year-end, your taxable profit reduces to 8,000 euros. That saves you around 1,055 euros in tax (8,000 x 26.375% = 2,110 euros instead of 12,000 x 26.375% = 3,165 euros). If you then reopen the position, you're still in the trade, but with a lower tax burden.

What to Watch Out For

Transaction costs, spread, and slippage eat part of the savings. In illiquid markets or wide spreads, the loss from re-entry can be larger than the tax savings. Calculate beforehand whether the trade is worth it.

Timing is important: Ideally, do this end of November or beginning of December, before the deadline for loss certificates on December 15. This gives you enough time to execute the positions cleanly. Good risk management is part of this: Don't close a position just for tax reasons if the trade still makes sense from a trading perspective.

Loss Offset in the GmbH

Loss offset works fundamentally differently in a trading GmbH than for private individuals. In the GmbH, there's no separate stock loss pot. All profits and losses flow into a single profit determination: Futures, stocks, options, CFDs, dividends, interest. Everything is offset without pot separation, without limitation.

The 20,000 euro cap for derivatives losses also never applied in the GmbH. The limitation exclusively affected private capital income under § 20 EStG. In the GmbH, trading profits are operating income and are subject to corporate tax (15%) and trade tax. This was one of the main reasons why futures traders set up a GmbH between 2021 and 2024.

Since the cap was abolished by the Annual Tax Act 2024, this specific advantage of the GmbH no longer exists. What remains: The GmbH offsets all losses in one pot, without separation between stocks and derivatives. For traders who actively trade both instrument classes, this can still be a relevant advantage. You can find all details on the GmbH decision in our article on starting a trading company in Germany.

FAQ: Loss Offset in Trading

Can I Offset Trading Losses with My Salary?

No. Capital losses can only be offset with capital income (§ 20 Abs. 6 Satz 1 EStG). An offset with income from employment, rental, business, or other income categories isn't possible. A loss deduction under § 10d EStG is also excluded for capital income.

Do My Loss Carryforwards Expire at Some Point?

No. Loss carryforwards for capital income are unlimited in time and amount. They're carried forward until you realize corresponding profits in the right pot. A loss carryforward from the stock loss pot remains until stock profits stand against it.

Can I Offset Losses from Crypto Trading?

That depends on the specific instrument. Leveraged crypto products (crypto CFDs, crypto futures) are capital income under § 20 EStG and fall into the general loss pot. Spot crypto that you hold less than one year is a private disposal transaction under § 23 EStG (with an exemption threshold of 1,000 euros since 2024) and has nothing to do with the loss offset pots for capital income. More on this in our article on trading taxes in Germany.

Our Tax & Finance module at United Daytraders covers loss offset in dedicated video lessons: from the offset pots to the loss certificate to concrete optimization strategies. Our Tax module with 4 lessons explains the differences between private individuals and GmbH structures in detail.