Trading Taxes in Germany: What International Traders Need to Know

Taxing trading profits sounds simple: 25% withholding tax, done. But as soon as you trade futures, want to offset losses, or think about a GmbH, it gets complex. The good news: The Annual Tax Act 2024 removed the most important restriction for futures traders.

This guide shows you the current situation in 2026, what trading taxes you have to pay in Germany, what you can deduct, which mistakes become expensive, and when your own company makes sense.

Tax Disclaimer: This article is for general information purposes only and does not replace individual tax advice. Tax regulations can change and depend on personal circumstances. Always consult a qualified tax advisor before making tax decisions.

How Trading Profits Are Taxed in Germany

Whether you buy stocks, trade CFDs, or trade futures, your profits are capital income. And capital income in Germany is subject to withholding tax.

That's the basic rule that determines everything else.

Withholding Tax: The Flat Rate

The withholding tax is 25%. On top comes the solidarity surcharge of 5.5% on the tax itself and, if you're a member of a church tax-collecting religious community, church tax.

Without church tax, you're at effectively 26.375%. With church tax, depending on the federal state, up to 27.99% (9% church tax) or 27.82% (8% church tax in Bavaria and Baden-Wuerttemberg).

In concrete terms for a trade: If you buy a stock for 1,000 euros and sell it for 1,500 euros, you pay a total of 131.88 euros withholding tax on the profit of 500 euros (without church tax). You keep 368.12 euros.

Transaction costs, meaning order fees and exchange charges, are deducted from the profit before tax is calculated.

The principle is deliberately simple: A flat rate, independent of your other income. Whether you earn 30,000 or 300,000 euros a year, you pay the same percentage on capital income. No progression, no income tax return for the tax itself necessary, at least in theory.

There's one exception: If your personal income tax rate is below 25%, you can request through the "more favorable test" that your capital income be taxed at the lower rate.

This is especially worthwhile for traders who have little other income, such as students, part-time workers, or traders who live exclusively from trading and are below the basic allowance.

German Brokers and Automatic Deduction

If you trade with a German broker, the tax is automatically withheld. Your broker deducts the corresponding amount directly to the tax office with every profit realization. At the end of the year, you receive an annual tax certificate and can declare the capital income in your tax return, but you don't have to if you don't want to claim a loss carryforward or similar.

With foreign brokers, it's different, more on that shortly.

Saver's Allowance: 1,000 Euros Tax-Free

Every taxpayer is entitled to a saver's allowance of 1,000 euros per year. For jointly assessed married couples, it's 2,000 euros.

Up to this limit, capital income is tax-free. Above that, withholding tax applies. To use the allowance, you set up an exemption order with your broker. If you have multiple brokers, you can split the amount.

Which Instruments Fall Under This?

Stocks, ETFs, CFDs, futures, options, certificates, dividends, interest: all capital income, all withholding tax.

It doesn't matter whether you hold a DAX ETF for years or do a hundred day trades a day with Nasdaq futures, the tax rate is identical. The differences are not in the tax rate, but in loss offset. And that's exactly where it got complicated in recent years.

Important to understand: Tax only applies upon realization. As long as you hold a position, unrealized profits are tax-free. Only when you sell does the profit become tax-relevant. This applies to all instruments equally. For futures and CFDs that are settled daily (Daily Settlement), each settlement counts as a realization, even if you hold the position overnight.

When Does Trading Become a Business?

A question that worries many traders: When does the tax office classify my trading as a commercial activity? The short answer: For proprietary trading with your own capital, practically never. You trade with your own money, on your own account, that's private asset management, not a business.

It becomes commercial when you trade for others, manage capital, or offer trading services. Pure proprietary trading, no matter how frequent or in what volume, remains private in most cases. There's no limit on the number of trades or trading volume at which private trading automatically becomes a business. Even full-time day traders who execute hundreds of trades daily remain tax-wise private investors as long as they trade exclusively with their own capital.

An important exception: Prop trading. We'll come to that below.

Loss Offset: The New Rules Since 2025

Loss offset was the most painful topic for active traders in Germany for years. Since 2025, the situation has fundamentally improved.

The Old Rule: The 20,000 Euro Cap (2021-2024)

With § 20 Abs. 6 Satz 5 EStG, the legislator introduced a limitation in 2021 that primarily affected futures and options traders: Losses from derivatives could only be offset with profits from derivatives up to 20,000 euros per year. Anything above that was carried forward, but in the following year also only up to 20,000 euros.

In practice, this meant: A trader who had 100,000 euros profit and 80,000 euros loss from futures, meaning net earnings of 20,000 euros, had to pay taxes on 80,000 euros because only 20,000 euros of the losses were creditable. The tax burden on the 80,000 euros: around 21,100 euros. With an actual net profit of 20,000 euros. An absurd situation that could drive traders with net profit into ruin.

Many futures traders therefore switched to CFDs, not because CFDs are better instruments, but because CFD losses didn't fall under the derivatives limitation. Others artificially reduced their trading volume or went abroad. The 20k cap was one of the biggest obstacles to professional futures trading in Germany.

The Annual Tax Act 2024: The Turning Point

With the Annual Tax Act 2024, in force since January 1, 2025, the 20,000 euro cap for derivatives losses was completely abolished. Losses from futures, options, and other derivatives can now be fully offset with corresponding profits since 2025.

This is the most important tax change for futures traders in years. Those who had switched to CFDs because of the cap or had artificially limited their volume can now trade futures again without tax disadvantage.

The Two Loss Offset Pots

What remains: The separation into two loss offset pots. Every trader must understand this.

Stock Loss Pot: Losses from the sale of stocks can only be offset with profits from the sale of stocks. Not with dividends, not with futures profits, not with interest. Only stock profits.

General Loss Pot: Losses from everything else (futures, CFDs, options, certificates) can be offset with each other and with dividends, interest, and other capital income. But not with stock profits.

In practice, this means: If you make 10,000 euros loss with stocks and 10,000 euros profit with futures, you can't offset these against each other. You pay around 2,638 euros withholding tax on the 10,000 euros futures profit, and the 10,000 euros stock loss is carried forward as a loss carryforward until you eventually realize stock profits. That's annoying, but unavoidable.

For active traders who mainly trade futures or CFDs, the general loss pot is the relevant one. Here, profits and losses can be freely offset against each other, across different instruments and asset classes. Only the stock pot remains isolated.

Loss Carryforward and Loss Certificate

Unoffset losses don't disappear. They are automatically carried forward to the next year as a loss carryforward. This applies unlimited, both in time and amount.

But be careful: If you have multiple brokers, each maintains its own loss offset pot. To offset losses across brokers, you need a loss certificate. And you have to request it from your broker by December 15 of the current year. Anyone who misses this deadline can only offset the losses with the same broker in the following year.

Practical Tip: If you trade various instruments, it can make sense to hold stocks and derivatives with different brokers. This avoids your broker trying to offset stock losses against derivative profits internally, which it can't do anyway, but which in practice can lead to delays and errors in settlement. Clean separation saves effort in the tax return and in risk management.

Important for Day Traders: Those who make many trades a day should keep an eye on their loss offset pots, not just at the end of the year. With German brokers, this happens automatically. With foreign brokers, you have to keep track yourself or regularly check the Activity Statements. Especially in volatile months where profits and losses alternate, this can make a significant difference in tax burden.

German vs Foreign Brokers: Tax Differences

The choice of broker has direct tax consequences. Not in the tax rate, that remains the same, but in the effort.

German Brokers: Convenient, But Limited

German brokers handle tax deduction for you. They calculate profits and losses, take the saver's allowance into account, deduct withholding tax, and provide you with an annual tax certificate. Tax-wise, this is the simplest way. You basically don't have to do anything except set up an exemption order and file the certificate at the end of the year.

Your broker also automatically maintains internal loss offset pots. Profits and losses within the account are offset against each other during the year before tax is deducted. In a bad quarter followed by a good one, you only pay taxes on the net profit without having to take care of it yourself.

The disadvantage: Many German brokers don't offer access to the platforms and instruments that professional traders need. Order flow tools, professional charting software, direct futures contracts at US exchanges, these aren't available or only to a limited extent with most German brokers.

Foreign Brokers: More Options, More Effort

Brokers like Interactive Brokers or AMP Futures don't deduct German tax. You're responsible yourself for declaring your capital income in your tax return via Annex KAP.

This means: You have to calculate your profits and losses yourself, fill out the correct forms, and pay the tax. The effort is higher, but manageable. Interactive Brokers, for example, provides detailed Activity Statements that break down all transactions, profits, losses, and fees. With this report, a tax advisor can prepare Annex KAP without much effort.

What you need to consider with Annex KAP: You enter your total capital income, divided into profits and losses, separated by the loss offset pots. withholding tax withheld abroad is credited. This can be relevant especially for dividends from US stocks or ETFs. Most foreign brokers provide the necessary information, you just have to transfer it correctly to the right lines of Annex KAP.

"Most of our traders use foreign brokers because of the better platforms, lower commissions, and direct access to futures markets. The additional tax effort is manageable if you have a tax advisor who knows this."

— Marco Bösing, founder of United Daytraders

Important: Just because your broker doesn't deduct tax doesn't mean the tax office won't find out. Through the automatic exchange of information (Common Reporting Standard, CRS), foreign brokers automatically report the account data of their German customers to the German tax authorities. Anyone who doesn't declare their foreign capital income risks tax criminal proceedings.

Prop Trading Taxes: A Special Case

Prop trading, meaning trading with the capital of a prop trading company, is a completely different category tax-wise. And that's exactly where many traders make expensive mistakes.

No Capital Income

The central difference: In prop trading, you don't invest your own capital. You trade with the company's money and receive a profit share, usually 70 to 90 percent of your profits. Tax-wise, these aren't capital income because you haven't invested your own money. Withholding tax doesn't apply. Many prop traders don't know this and declare their income incorrectly, with expensive consequences.

The Tax Classification

Prop trading income is usually classified as other income under § 22 EStG or as commercial income under § 15 EStG. The distinction isn't conclusively clarified and depends on the specific structure: How independent are you? How regular? Which platform do you use?

The consequence: Instead of the flat 25% withholding tax, the progressive income tax rate applies, up to 42% plus solidarity surcharge. With high income, you pay significantly more than with withholding tax.

Business Registration and Deductibility

If your prop trading activity is classified as commercial, you need a business license. This brings obligations (trade tax, IHK membership), but on the other hand you can deduct business expenses. Challenge fees you pay to the prop trading company are usually deductible, as are hardware, software, and other directly attributable costs.

The advantage over private capital income: As a business operator or with other income, you can deduct all directly attributable expenses from your income. This includes not only challenge fees, but also your trading computer, monitors, internet costs (proportionally), further education, and even a home office. This deductibility doesn't exist with withholding tax.

Legal Situation in Flux

The tax treatment of prop trading isn't a settled issue. There's no clear BFH case law, and tax offices handle the classification differently. Some tax offices accept classification as other income, others insist on a business. The consequences are significant: Trade tax, social security obligation, IHK contributions, all of this depends on the classification.

A tax advisor with experience in this area isn't optional, it's necessary. Anyone who taxes their prop trading income without professional advice risks paying either too much or too little, and both have consequences. More on this topic in our article on prop trading taxes.

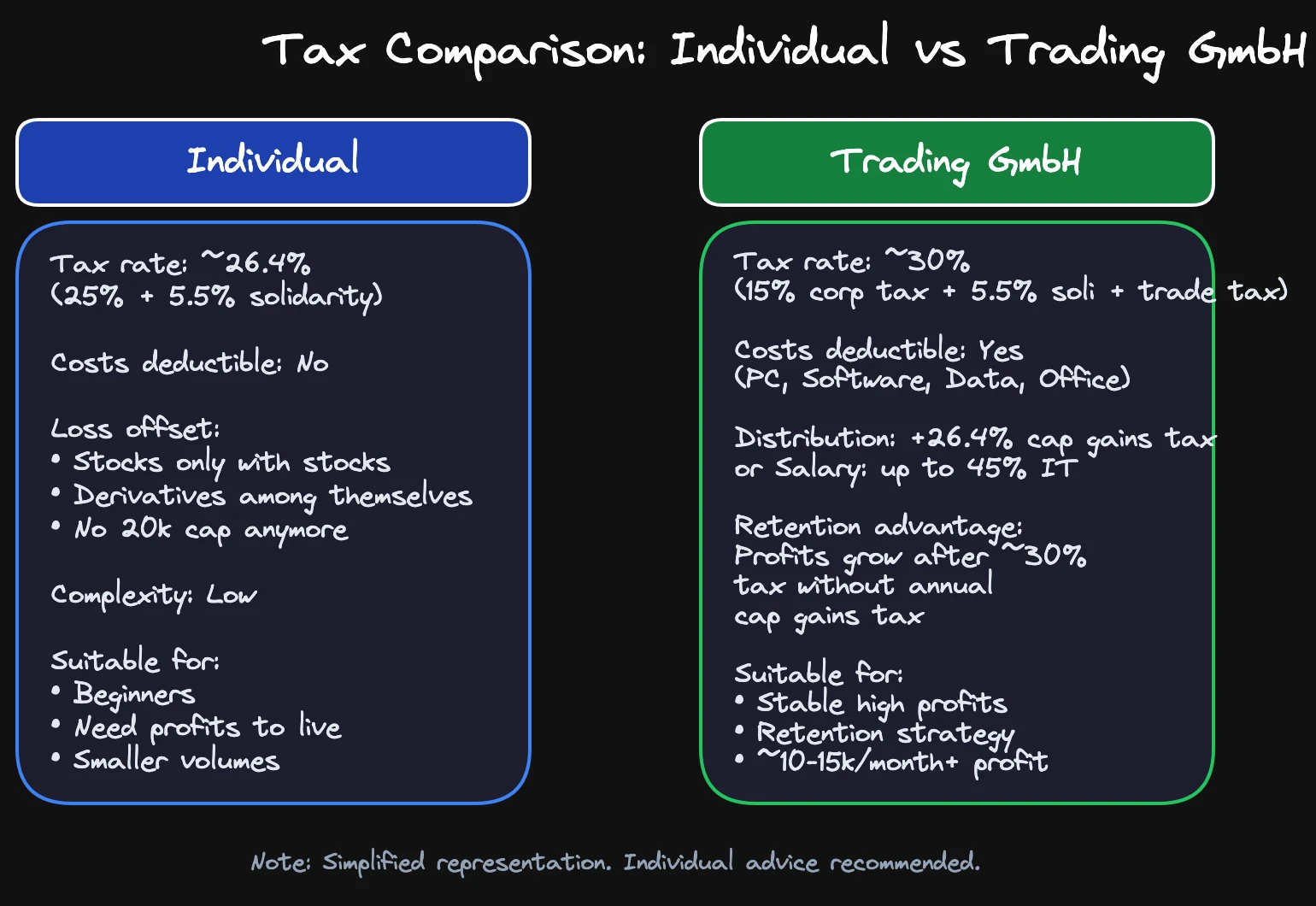

Private or GmbH: The Decision

At a certain profit level, every trader faces the question: Does my own company make sense? The answer is less clear-cut than many YouTube videos suggest.

Private: Simple and Cheap, With Limits

As a private individual, you pay 26.375% on your capital income. Flat, simple, done immediately. No bookkeeping, no tax advisor necessary, at least not with a German broker. The disadvantage: You can't deduct any costs. No computer, no data feeds, no office, no further training. Tax is due on the entire profit.

GmbH: More Options, More Complexity

A trading GmbH pays around 30% tax on its profits: 15% corporate tax plus 5.5% solidarity surcharge on the corporate tax and approximately 14-17% trade tax (depending on your municipality's rate). At first glance, more than private withholding tax. On top come ongoing costs: Tax advisor, bookkeeping, IHK contributions, business account. Expect 200 to 500 euros per month just for administration.

And it gets worse when you want to withdraw money from the GmbH. With a profit distribution, another 25% capital gains tax plus solidarity surcharge applies. With withdrawal via salary, your personal income tax rate applies, up to 42% plus solidarity. The total burden with immediate withdrawal is therefore significantly higher than private withholding tax.

The advantage lies elsewhere: Cost deduction and retention. In the GmbH, you can deduct all professional costs: PC, software, data feeds, office, company car, further training. And the real advantage: If you leave profits in the GmbH and reinvest them, your capital grows after one-time taxation at around 30% without annual capital gains tax on realized profits within the company. Over decades, this retention advantage creates a massive wealth difference.

Another aspect that many overlook: The GmbH offers legal certainty. In recent years, the legislator has tightened the taxation of private capital income several times, the 20k cap for derivatives was the most prominent example. The GmbH wasn't affected by this. Those who plan long-term appreciate this stability.

The Core Question

It depends on what you do with the money. If you need your trading profits to live on, private is almost always cheaper. If you want to build capital and reinvest profits, the calculation turns in favor of the GmbH at a certain point.

As a rough guide: From about 10,000 to 15,000 euros monthly trading profit, with consistent retention and relevant deductible costs, the GmbH starts to make sense. Below that, the fixed costs eat up the tax advantage.

One thing is clear: The GmbH isn't a beginner's topic. Those still learning to trade consistently profitably don't need a company, but focus on their trading. The GmbH is the optimization tool for the point when profits are stable and high enough to justify the additional complexity. Details on formation, costs, and the honest calculation can be found in our article on starting a trading company in Germany.

Optimizing Trading Taxes: What's Allowed

Tax optimization isn't a trivial offense, it's your right. As long as you stay within the law, there are several levers to reduce your tax burden as a trader.

Exhausting the Saver's Allowance

Sounds trivial, but is often forgotten: Set up an exemption order with your broker. 1,000 euros capital income per year is tax-free, that's 264 euros saved tax at 26.375%. For married couples, double that. Distribute the allowance sensibly if you have multiple accounts.

Tax-Loss Harvesting

At year-end, sell positions with unrealized losses to reduce realized profits, and rebuild the position directly after. In Germany, there's no strict wash-sale rule like in the US. You can sell a stock and buy it back the next day without the loss being denied for tax purposes. Pay attention to assignment to the correct loss pot: Stock losses only against stock profits, derivative losses against the general pot.

Involving Your Spouse

If your spouse doesn't exhaust their own saver's allowance, joint assessment or a joint account can double the available allowance. A transfer of positions with high unrealized profits to the spouse can also make tax sense, but discuss this with a tax advisor.

Timing: The December Strategy

Profits and losses are offset on an annual basis. Towards year-end, it's worth looking at the balance: If there are high realized profits, it can make sense to realize loss positions in December. Conversely: With high losses, you can consciously push profits into the new year, for example by closing profitable positions only in January.

This strategy works particularly well with swing positions that you would evaluate at year-end anyway. With day trading, the effect is more limited because positions are closed daily. Still: Taking a conscious look at the tax balance in early December and planning the last weeks accordingly can save several hundred or thousand euros in taxes.

What the GmbH Can Do That You Can't Do Privately

Training costs, trading software, hardware, office: As a private individual, you can't deduct any of this from your capital income. In the GmbH, all of this is deductible. This is one of the main reasons why traders with high ongoing costs consider a company.

The Boundary: Avoidance Isn't Evasion

Tax avoidance, meaning the legal use of all structuring options, is allowed and sensible. Tax evasion is a criminal offense. The boundary in practice is clear: Declare all income correctly, follow all regulations, don't conceal accounts or income. Anyone who follows the rules can optimize as much as they want.

Concretely: Setting up an exemption order is tax avoidance, allowed. Tax-loss harvesting is tax avoidance, allowed. Setting up a GmbH to deduct costs and retain profits is tax avoidance, allowed. Not declaring capital income from a foreign broker in your tax return is tax evasion and is punished.

The Most Common Tax Mistakes by Traders

Tax mistakes not only cost money, they can result in criminal proceedings. These six mistakes we see again and again.

1. No Tax Return with Foreign Broker

The most common and most dangerous mistake. Anyone who trades with Interactive Brokers or another foreign broker and doesn't declare their profits in their tax return is committing tax evasion. Through the automatic exchange of information (Common Reporting Standard, CRS), brokers in over 100 countries automatically report their customers' account data and income to their home tax authorities. The German tax office knows you have an account, what your balance is, and what income you've earned. It's not a question of whether they find out, but when. The penalty for tax evasion: Up to five years imprisonment or fine, plus back payment, plus interest.

2. Forgetting Loss Certificate

Anyone who trades with multiple brokers and wants to offset losses across brokers must request a loss certificate by December 15. Anyone who misses this deadline can only offset losses with the same broker in the following year and potentially loses a whole year of tax optimization.

3. Mixing Stock and Derivative Losses

The two loss offset pots aren't optional, they're law. Stock losses can only be offset with stock profits, everything else only with each other. Anyone who does this wrong in their tax return risks a correction by the tax office and potentially a back payment with interest.

4. Treating Prop Trading Like Capital Income

Prop trading income isn't capital income. Anyone who declares it as such and pays only 25% withholding tax is wrong. The consequence can be retroactive taxation at the full income tax rate, plus interest and late payment surcharge.

5. Founding a GmbH Too Early

The trading GmbH is an optimization tool for profitable traders with high, stable profits. Anyone who sets up a GmbH before they're consistently profitable pays monthly fixed costs for tax advisor and bookkeeping without value. 25,000 euros share capital tied up, ongoing costs of 200 to 500 euros per month, double-entry bookkeeping obligations, and then in a loss month no income but still having to pay the fixed costs. First become profitable, then optimize.

6. Not Using a Specialized Tax Advisor

A normal tax advisor knows about real estate and businesses, not about derivatives, loss offset pots, and the tax classification of prop trading. A tax advisor without trading experience can end up costing you more than they save. We've seen cases where tax advisors recommended the wrong loss offset to their clients or didn't even know there are two separate pots. Invest the time to find a specialist, ask for recommendations in trading communities, or inquire directly whether the advisor has experience with futures, order flow trading, and derivatives.

FAQ: Trading Taxes Germany

How Much Tax Do I Pay on Trading Profits?

As a private individual, you pay 26.375% withholding tax (25% plus 5.5% solidarity surcharge) on all capital income above the saver's allowance of 1,000 euros. With church tax, up to 27.99%. The tax rate is flat and independent of your other income. Exception: Prop trading income, which is subject to the progressive income tax rate.

Do I Have to Tax Myself with a Foreign Broker?

Yes. Foreign brokers don't deduct German tax. You're obliged to declare your capital income via Annex KAP in your tax return and pay the tax yourself. Most foreign brokers provide detailed reports that serve as the basis for the tax return. Through the automatic exchange of information (CRS), the tax office learns about your account, non-declaration is tax evasion.

Can I Offset Trading Losses with Profits?

Yes, but with restrictions. Stock losses can only be offset with stock profits. Losses from futures, CFDs, options, and other derivatives can be offset with each other and with dividends, interest, and other capital income, but not with stock profits. The 20,000 euro cap for derivatives losses was abolished in 2025. Unoffset losses are carried forward unlimited. More details in our article on trading loss offset in Germany.

Do I Need a Tax Advisor as a Trader?

If you trade with a German broker with small volume, you can get by without a tax advisor. But as soon as you trade with a foreign broker, move high volumes, want to offset losses, or think about a GmbH, a specialized tax advisor is the best investment you can make. Make sure they have experience with trading and financial instruments, the subject is too specialized for a generalist.

Our Tax & Finance module with 4 lessons explains the differences between private individuals and GmbH structures in detail. At united-daytraders.com, you'll find the module alongside over 1,500 video lessons from institutional traders.