Settlement Price: The Forgotten Reference Level in Day Trading

Settlement price is the official closing reference price for futures contracts, set by the CME each trading day. It is not determined by the last traded price but as a volume-weighted average of the final 30 seconds of the trading session. This difference matters more than most retail traders realize.

Risk disclaimer: Trading futures and other financial instruments carries significant risk of loss. Past results are not indicative of future performance. Only trade with capital you can afford to lose.

What Settlement Price Actually Is

Most retail traders don't even know this price exists. They look at the "last traded price" or "close" on their charts without realizing that institutional accounts are evaluated against a completely different price — the settlement. This isn't a technical detail that only concerns accountants. It determines how trillion-dollar portfolios are valued every single day.

Calculation and Exchange Logic

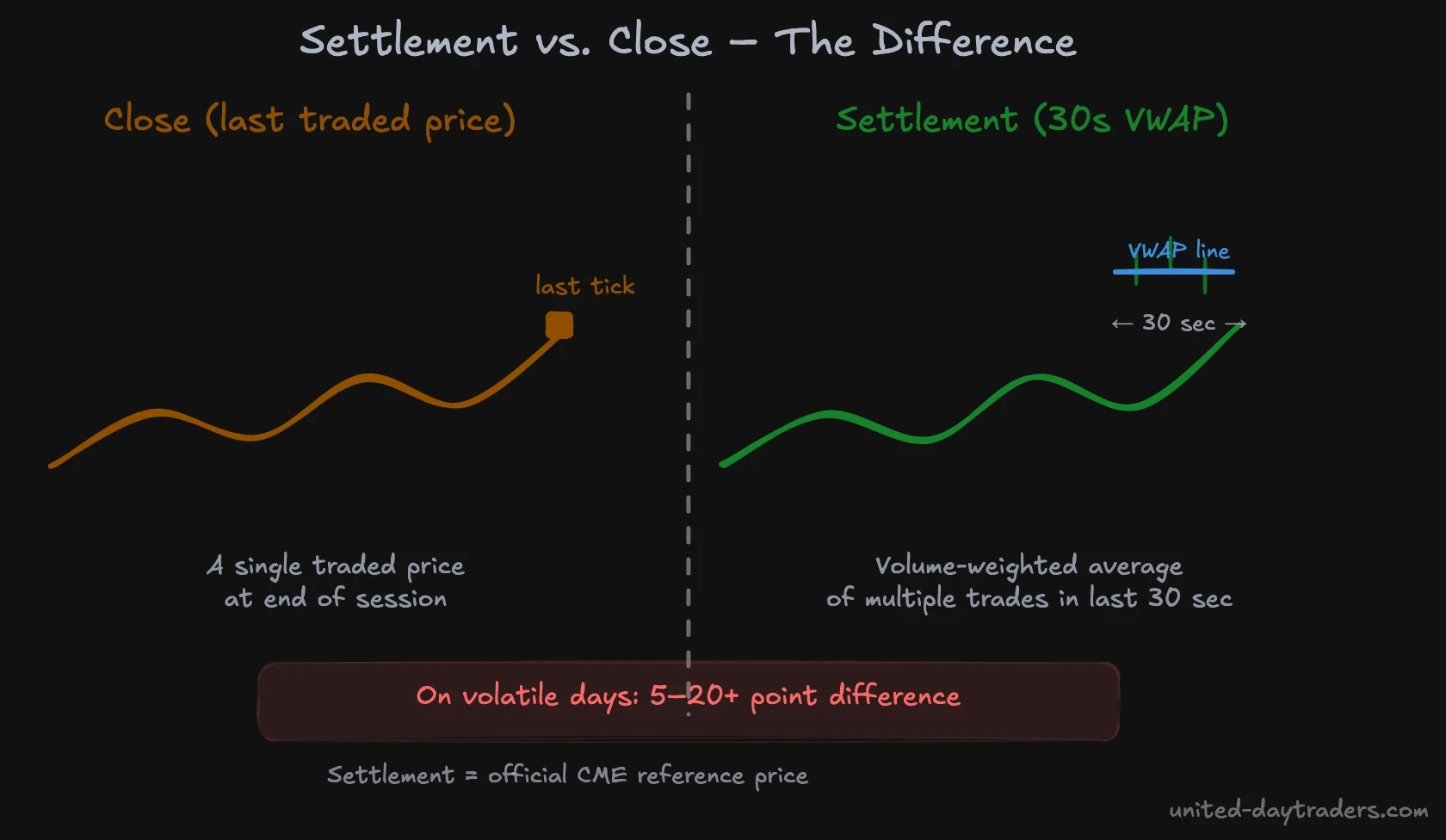

The CME calculates settlement as a volume-weighted average of all trades during the final 30 seconds of the Regular Trading Hours session. For NQ futures, that means the last 30 seconds before the cash close at 4:00 PM ET (3:59:30 to 4:00:00 PM ET). The settlement price is thus fixed shortly before the daily trading halt (which runs from 4:15 to 4:30 PM ET). This is explicitly NOT the 4:15 PM electronic close that most retail traders see on their charts.

The methodology serves a clear purpose: settlement cannot be manipulated by a single large order placed in the last few seconds. Because it takes a volume-weighted average across 30 seconds, a trader dumping contracts right before the bell has minimal impact on the final settlement figure. This makes settlement a fairer and more stable reference point than the last traded tick.

Settlement vs. Close: The Difference Matters

Most charting platforms display the "close" as the last traded price in the main session. On volatile days, this can differ significantly from the settlement price. On expiration days or high-volatility sessions, the difference between settlement and close can be 5–20 or more NQ points.

Why this matters practically: if you check "where price closed" on your platform and compare it to settlement, and they differ by 10 points, you are looking at the wrong level for institutional analysis. Settlement is authoritative. The close is just the last tick.

Tip: Most professional platforms (e.g., Sierra Chart, CQG) display a separate "SETTLE" line on the daily chart. The CME Group publishes daily settlement prices on their website.

Why Institutional Traders Watch Settlement

Institutional accounts — prop desks, hedge funds, pension funds — are evaluated against settlement, not against the last traded price. This creates specific behavioral patterns around settlement:

-

Margin requirements: Futures margin is calculated from settlement. A position losing $50K based on the last tick might be evaluated against settlement as only losing $30K if settlement is more favorable. This matters for overnight margin calls.

-

P&L reporting: Institutional P&L is marked to settlement daily. A desk that ended the day at +$200K based on the last tick, where settlement shows only +$150K, reports +$150K. Settlement IS the day's result in institutional terms.

-

Position evaluation: When a portfolio manager reviews risk at end of day, they use settlement. The settlement level is therefore the price at which the most institutional decision-making takes place.

The consequence: price gravitates back toward settlement because many institutional participants are anchored to it.

Using Settlement as a Trading Level

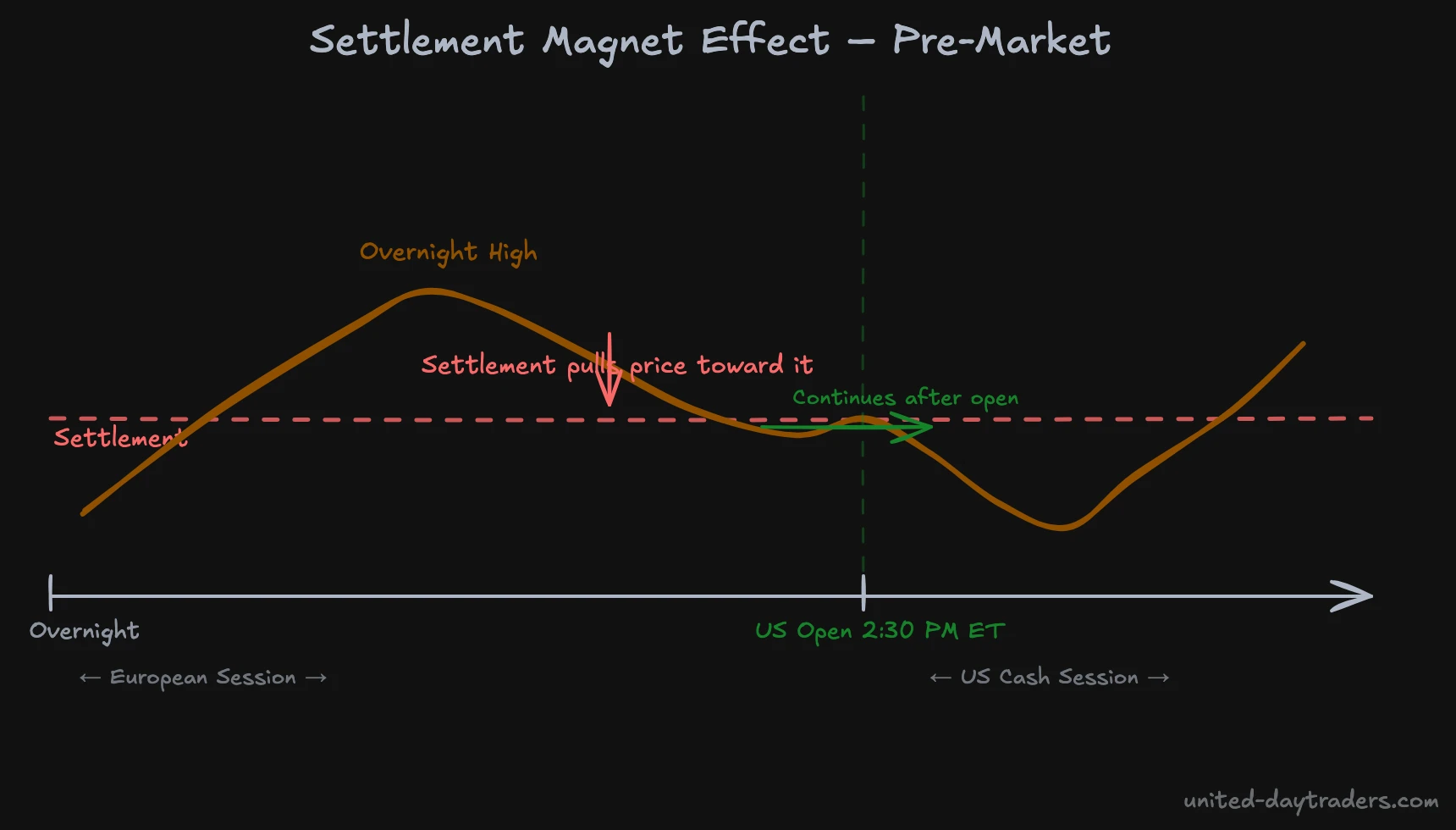

Magnet Effect During Pre-Market

The most actionable insight: settlement often acts as a magnet during the European pre-market session (before the US cash open at 2:30 PM CET). Price that gapped away from settlement overnight tends to get tested back to settlement before or shortly after the regular session begins.

This is especially consistent in NQ futures:

- If overnight price runs far above settlement, watch for a test back to settlement before or shortly after the US open

- If overnight price is far below settlement, there is often a bounce attempt toward settlement early in the European session

This magnet effect is not guaranteed but adds a statistical tilt: when you are in a trade and settlement is 30 points away, price often pulls toward it before moving further. Use settlement as a partial target or decision point.

More on session-based reference levels: Session High Low in Trading

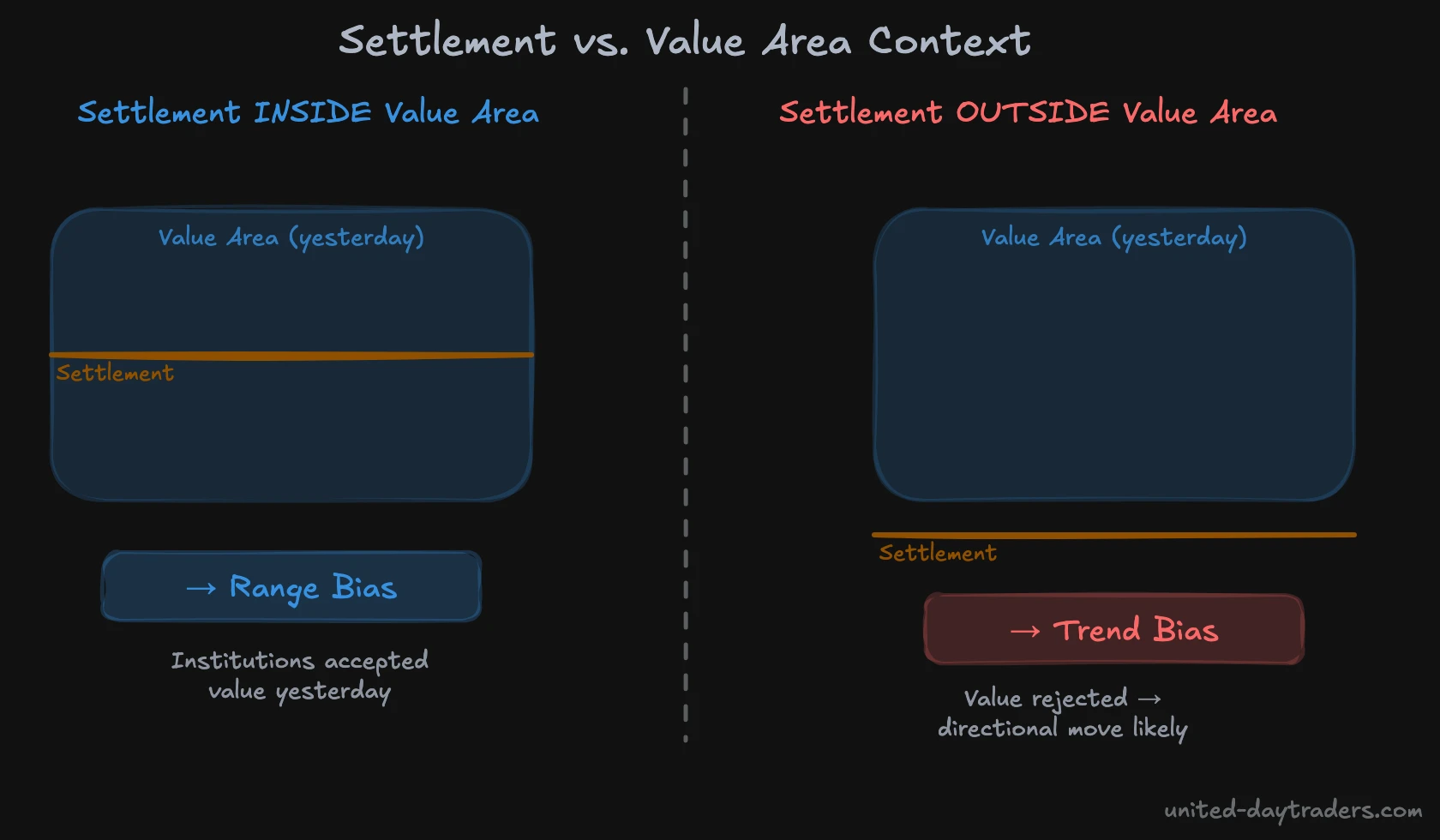

Settlement in Value Area Context

Settlement gains additional meaning when viewed alongside the previous day's Value Area from the Volume Profile:

Settlement inside yesterday's Value Area:

- The market accepted value at settlement level

- No strong directional pressure from institutions

- Range day probability increases

- Fade breakout attempts, target value area boundaries

Settlement outside yesterday's Value Area:

- The market did not accept value at settlement level — it moved away

- Institutional participants who marked P&L at settlement may look to either exit or add positions

- Trend day probability increases

- Trade with the direction away from VA

This context transforms settlement from a single number into a regime indicator: inside VA equals range bias, outside VA equals trend bias.

For more on this framework: Auction Market Theory in Trading

How to Find and Mark Your Settlement Price

Step by step:

- CME Website: Go to CME Group → Quotes → Find your contract (e.g., NQ futures). Daily settlement prices are published after session close.

- On Sierra Chart: Settlement appears as a horizontal line labeled "SETTLE" on the daily chart. Most institutional data providers include it by default.

- On TradingView: Search for the continuous futures contract. Settlement is often labeled but may differ slightly from the official CME figure — always verify against CME directly for critical decisions.

- Mark it on the daily chart: Draw a horizontal line at yesterday's settlement every morning before trading. This is a 30-second routine that adds institutional-grade context to every trade you take.

FAQ

Is there a settlement price for every trading day?

Yes, the CME calculates a settlement price for every futures contract every trading day. For NQ futures, it is published daily after the end of Regular Trading Hours (3:15–3:30 PM ET). Different rules may apply on weekends and exchange holidays.

Why does settlement sometimes differ significantly from the last traded price?

Because settlement is a VWAP of the last 30 seconds, not the last tick. On days with high volatility or unusual end-of-day order flow (e.g., index rebalancing, options expiry), the final seconds can deviate sharply from preceding prices, which separates the settlement VWAP from the closing tick.

Should I actually mark the settlement price every day?

Yes, especially if you trade NQ futures. The 30 seconds per day you spend marking settlement gives you a level that institutional traders are watching. It is one of the most asymmetric time investments in trading.

Settlement is a core component of the daily market analysis in the traMADA NQ Masterclass. Across 1,500+ video lessons, you learn how to combine settlement, value area, and session levels into a complete institutional picture. Visit united-daytraders.com for the full program.