Risk Management in Trading: Position Sizing and Stop-Loss Placement

Risk management in trading doesn't start with position size, it starts with stop-loss. Most retail traders do it backwards: they choose a position size and then set an arbitrary stop. Institutional traders first define where their thesis breaks, and only then calculate position size. The difference between both approaches decides whether you stay in the game long-term or blow up your account at some point. Anyone who has understood trading psychology knows: fear and greed sabotage exactly this process, and good risk management is the technical protection against it.

Risk Warning: Trading futures and other financial instruments carries substantial risk of loss. Past performance is not indicative of future results. Only deploy capital you can afford to lose.

Why most traders approach risk management wrong

The classic beginner mistake looks like this: a trader decides on 2 contracts, opens the trade, and then puts a stop-loss somewhere, maybe 100 points away, maybe 20. The position size is already set before the risk is even defined. That's like setting your bet at the poker table before looking at your cards.

Institutional traders reverse the process. First comes the question: where is my thesis invalid? At what price level does the trade not make sense anymore? Only when this point is established is the position size calculated, backwards, starting from the maximum loss you're willing to accept. If you want to systematically evaluate your results, you need a good trading journal for that.

"In trading it's about one thing: protect your money first. The longer you stay in the game, the more your core process takes effect."

— Marco Bösing, founder of United Daytraders

The "100-point stop" is a myth. A stop-loss that's always the same distance away ignores market structure completely. If your stop is 5 ticks below a swing low, you're protected. If it sits in the middle of nowhere, it's just a wish. Trading psychology explains why fear makes traders set stops too tight or too wide. Risk management is the technical answer to this emotional problem.

The position sizing formula: the 1-2% rule

The basic rule is: never risk more than 1-2% of your account balance per trade. At United Daytraders we often work even more conservatively and risk only 0.2-0.5% per trade. That sounds small, but it has a decisive advantage: you survive losing streaks without your account shrinking significantly.

The formula for position size is simple:

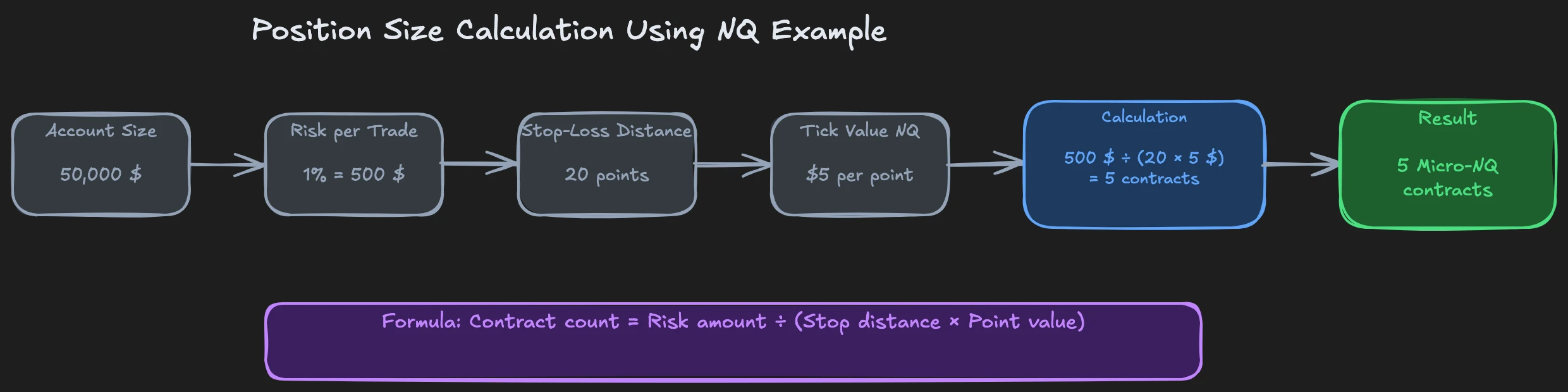

Position size = Risk budget ÷ (Stop distance × Point value)

A concrete example: you have a $10,000 account and want to risk maximum 1%, that's $100. Your stop-loss is 20 points away in the Nasdaq future. A micro contract (MNQ) has a point value of $2. So: $100 ÷ (20 × $2) = 2.5, you can trade 2 MNQ contracts.

Second example: $25,000 account, 1% risk = $250. Your stop in the E-mini S&P 500 is 10 points away. An ES contract has a point value of $50. So: $250 ÷ (10 × $50) = 0.5, you can't even trade one full contract. The honest answer: you skip this trade or switch to the micro contract (MES, point value $5), where you could trade 5 contracts.

When the formula tells you that you can't take the trade, that's exactly risk management. The discipline to skip a trade protects your capital more than any strategy. Think in percentages, not in dollars, because in a drawdown you automatically risk less in absolute numbers, and in a winning streak automatically more. That's built-in compounding.

R-multiples: Think in risk, not dollars

An R-multiple is the universal language of risk management. 1R is your risk per trade, the amount you lose if your stop-loss gets hit. A profit of 2R means you earned double your risk. A 5R winner brings five times. The concept was popularized by Dr. Van K. Tharp in his book "Trade Your Way to Financial Freedom."

Why is this useful? Because it makes your performance comparable across different instruments and account sizes. $200 profit sounds good, but as 0.5R it's mediocre. $50 profit sounds modest, but as 3R it's excellent.

Imagine a typical trading week: Monday -1R, Tuesday -1R, Wednesday -1R, Thursday +3R, Friday +5R. The result: +5R net, with only 40% hit rate. Three losers, two winners, still clearly in the green.

"Trading is like a business: we invest small, small, small again and again, and when we win, we win significantly bigger."

— Marco Bösing, founder of United Daytraders

A single good trade often brings more than four losses combined. That changes the perspective: a small loss isn't failure, but the cost of being present in the market. A healthy equity curve looks exactly like this: small dips down, then bigger jumps up.

Setting stop-loss correctly

A stop-loss belongs where your trading thesis becomes invalid, not where you feel emotionally comfortable. That's a fundamental difference.

Wrong: Always 10 points stop, no matter what the chart looks like. A fixed stop ignores market structure and gets triggered either too early or too late.

Right: The stop is below a structure level: a swing low, a value area, a VWAP, or the zone of a big trade. When the price breaks through this level, the market logic has changed and your trade doesn't make sense anymore.

There's a trade-off: tight stops mean you'll get stopped out more often, but the individual losses are smaller. Wide stops keep you in the trade longer, but cost more when they trigger. In my experience, tighter stops with willingness to re-enter work better. The logic: getting stopped out three times at 0.2% and earning 1R on the fourth attempt is better than losing 1% once.

For the exact calculation of tick values for various futures contracts you need the contract specifications. One tick in ES is $12.50, in NQ $5.00, in MNQ $0.50. These values flow directly into your position sizing formula.

Scaling: Increase winning trades

Scaling is the multiplier that makes good risk management excellent. The principle: when your trade is in profit and you move your stop to break-even, your monetary risk is zero. In this moment you can open a second position without increasing your total risk.

The calculation: you open a trade with $100 risk. The trade runs 1R into profit, you move the stop to break-even. Now you add a second contract on a pullback. Your average entry price shifts, but your stop protects both positions. If the trade continues, you earn double, with an original risk of $100.

"Now I've created the enormous potential of risk equal to zero. If the trade continues for me, I win double. That's a booster for your account."

That's the exact opposite of what most retail traders do. They increase losing positions hoping the market turns. Scaling into winners reverses the logic: you only increase what's already working.

Scaling into losers isn't fundamentally wrong, but only when the maximum total loss is defined beforehand. Example: you plan 0.5% risk, but start with only 0.25% and reserve the possibility to add at a better price within your planned zone. That's a calculated approach with a fixed maximum. What must never happen: loading into a loser uncontrollably without knowing where it ends.

The complete scaling methodology requires confirmation signals through order flow analysis and footprint charts. Without this confirmation, scaling is a guessing game. But here we're talking about the basic principle: increase winners, limit losers. That's the essence of profitable trading.

FAQ: Risk Management in Trading

How much percent to risk per trade?

For retail traders, 1-2% per trade is a solid starting point. At United Daytraders we often work with 0.2-0.5% per trade because we calculate with the compounding effect over weeks and months. What matters less is the exact number than the consistency to maintain it on every trade, especially and particularly after losing streaks.

What's a good risk-to-reward ratio?

Minimum 1:2, ideally 1:3 to 1:5. With tight, structure-based stops and willingness to let winners run, such ratios are realistic. A 1:1 ratio only works with a hit rate above 50% (in practice more like 55%+ because fees and slippage add up), and few traders maintain that consistently.

Should I trail my stop-loss?

Yes, but structure-based, not arbitrary. After 1R profit you move the stop to break-even. After that you orient yourself on swing lows (for long trades) or swing highs (for short trades). Time-based or emotional trailing leads to cutting winners too early.

Our 30-day "Building a Trader" program trains exactly these skills systematically: from correct stop-loss through position sizing to scaling strategies. In the Trader Framework course we dedicate 8 separate lessons to money management. At united-daytraders.com you'll find the program together with over 1,500 video lessons from institutional traders.